This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It’s a tough time for a lot of startup founders right now. Many companies are now having to resort to tough measures in order to stay afloat, including layoffs, downrounds and tough terms from current investors. What is a founder to do? If the answer is yes, then a downround is likely the best path forward.

The past year was a wild ride for startups and founders, giving a whole new meaning to the ”rollercoaster” aspect of being an entrepreneur. The press took notice, especially since just a few months later startups were laying off employees en-masse to cut costs. Sustainable growth: Prioritise sales efficiency over growth at all costs.

The A round was done in February 2000 (end of the bull market) and my B round was done in April 2001 (bear market). As a result I had to do a downround. Downrounds are psychologically really difficult on companies and can make it harder to do later rounds. I eventually needed more money.

” In the article I discussed the downside of raising capital at a too high of a price and referred people to a previous article I had written encouraging founders to raise “ At the Top end of Normal ” as opposed to stratospheric prices. The Damaging Psychology of DownRounds. A downround.

In times when venture capital is hard to get, investors extract high costs for failure (down-rounds, cram downs , new management teams, shut down the company.) Sales people cost money, and when they’re not bringing in revenue, their wandering in the woods is time consuming, cash-draining and demoralizing.

I recently spoke at the Founder Showcase at the request of Adeo Ressi. I said that at the Founder Showcase, too. And for many of these they were (over) funded 7-10 years ago and don’t necessarily all represent great returns for investors or founders. New investors hate downrounds. That’s a fact.

A founder asked me what makes a $2M round “pre-seed”? And why do we still sometimes hear about pre-seed rounds that look more like a series A in pricing and size? What’s the difference between an angel round and pre-seed round and why do I believe we’ll see more pre-seed rounds taking place in 2024?

The smartest companies in the market that I know are working aggressively to lower burn rates through pragmatic cost cutting knowing that the next fund-raising cycle may be unpleasant. I’ve heard enough companies say “we simply can’t cut costs or it will hurt the long-term potential of the business” to get a wry smile.

It is going to cost a lot of money just to get the initial batch of products to test the market and would definitely require external funding. I have interacted with a lot of founders who funded their initial business expenses through credit cards. You might have seen that valuations of several unicorns were suddenly slashed down.

The founders were very sympathetic; a man, laid off from his job, and his very pregnant wife, who sold their house and investing $150k into the business and are working hard to make a go of it. The two founders invested $40k in the business, and plan to license it rather than manufacture it because manufacturing seems too hard.

Type to Add and Search Questions; Search Topics and People Startups Startup Compensation Entrepreneurship Compensation Stock Options Major Internet Companies Silicon Valley Why is there such a large founder to early employee equity drop-off? The real question here is: why is it fair for founders to get so much more?

One of my favorite lines in buried in the middle: “I’ve heard enough companies say “we simply can’t cut costs or it will hurt the long-term potential of the business” to get a wry smile. Pragmatic cost cuts are always possible and often productive.” I have two simple rules for founders in my head from this experience.

And people like Jeff Clavier, Aydin Senkut, Dave McClure, Chris Sacca & Eric Paley (at Founder Collective) are leading the charge. Chris Sacca talked about how a $20 million exit can change a founder’s life and that shouldn’t be scoffed at. That’s awesome. I had two kids and a rental house.

Founders Institute Plain Preferred Term Sheet (by WSGR – disclaimer, I represent the Founders Institute and was involved in drafting this document). Yes for Series Seed holders and founders. Y Combinator Series AA Equity Financing Documents (by WSGR). Series Seed Financing Documents (by Fenwick & West). Drag-along.

Why Inside Rounds are Difficult? Many founders don’t understand why inside rounds are so difficult. So inside rounds get delayed and when there are non-participants you often find “recaps” or “structure” or “pay-to-play” provisions. Why DownRounds are Harder Than You May Think.

Many startups extended runway, cut costs and took on painful downrounds or expensive debt to avoid raising in 2023. It’s not just a cost consideration, but a desire for independence and neutrality. Those ‘band aids’ are running their course and it might get worse (i.e.

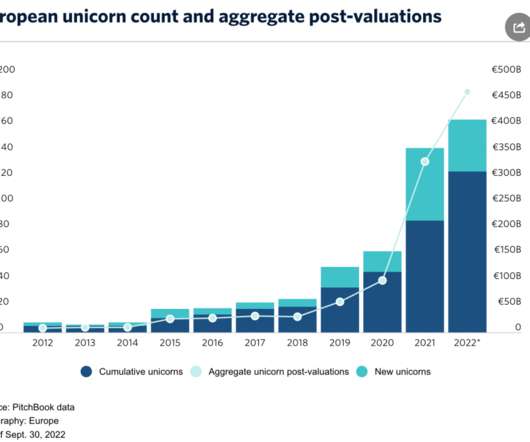

The 2022 Founders Factories report by DealRoom and Accel shines a spotlight on the startup clusters that produced most unicorns across Europe and Israel, and then tracks the alumni of those unicorns to test where the talent goes to found their next companies. London and Tel Aviv are home to the most founder nurturing unicorn startups.

The statistics show that even though most founders bet their time and resources that their startups will be the best in the world, 90% of those new startups won’t be in operation in 10-15 years. For example, “How will unit cost affect our capital requirements and how will product pricing affect revenue?”

Technical progress and market traction are much slower and cost a lot more than anticipated. Usually unbeknownst to all, the decision around pursuing or accepting a venture capital round will be the most important factor in determining the investment return for the founder and the original angel investors in the company.

In other words, it isn’t that VCs suddenly got smart, it’s that the costs of starting a company went down dramatically. Angels / seed often wanted to exit early and late-stage wanted more ownership than founders would sell so secondary transactions were common. 3VCs agreed to fund an inside round and cut costs.

Investors sat with the founder & CEO, Jason Spievak, and asked him what he wanted to do about the future. Like the market, Invoca has learned the importance of pragmatic growth over “growth at all costs” because when markets shift companies that run lean always have more options than those that only have a growth agenda.

This is only a minor problem in that both forms can convert easily into ‘C’ corporations at low cost and little consequence. Second, it is important in the first investment round to face the issues that may be required later by subsequent, more sophisticated, investors such as VC’s.

by Michael Woolf that is worth any startup founder reading to get a sense of perspective on the reality warp that is startup world during a frothy market such as 1997-1999, 2005-2007 or 2012-2014. So if your costs are $500,000 per month and you have $350,000 per month in revenue then your net burn (500-350) is equal to $150,000.

This is only a minor problem in that both forms can convert easily into ‘C’ corporations at low cost and little consequence. These include “tag along rights” which allow investors to sell some shares when others, such as management or founders, sell any shares. And what VC’s worry about.

Likely signs of a Value investment: the company has challenges in filling out the round; the investors have more negotiating leverage than the founders during the closing process; the company has significantly better metrics (e.g. The reverse also holds: a Value investment can become Momentum, and then follow with a downround.

The second round is often for some or all of the following – corporate growth, go to market, turn the prototype into a robust offering, marketing costs, or to hire a sales force. It’s no longer based on a hunch, unless the company is in trouble and needs money to finish what the first round started. Founders Fund.

Later stage funds will end up owning more of their portfolio companies via downrounds and ultimately should see ok returns. The early stage investors are going to take a huge hit since many of their portfolio companies will be capital starved and will be forced out of business or into fire sales. But some will be saved.

What most managers miss is that every month cut from the time it takes to perform such tasks cuts the cost by the value of a month’s worth of fixed overhead or burn. Ignoring the cost of product for a moment to make a point, saving a month’s fixed overhead by making processes more efficient, could easily double profits for the year.

A typical startup goes throughseveral rounds of funding, and at each round you want to take justenough money to reach the speed where you can shift into the nextgear. I think it would help founders to understand funding better—notjust the mechanics of it, but what investors are thinking. Few startups get it quite right.

And now I have to explain to team that they’re taking more dilution than they expected if we do a downround. A downround? I know how to structure around that to protect the founders from getting screwed on a multiple liquidation preference. Raising lower seems kind of like something is wrong.

What most managers miss is that every month cut from the time it takes to perform such tasks cuts the cost by the value of a month’s worth of fixed overhead or burn. Ignoring cost of product for a moment to make a point, saving a month’s fixed overhead by making processes more efficient, could easily double profits for the year.

What most managers miss is that every month cut from the time it takes to perform such tasks cuts the cost by the value of a month’s worth of fixed overhead or burn.

All Unicorn participants — founders, company employees, venture investors and their limited partners (LPs) — are seeing their fortunes put at risk from the very nature of the Unicorn phenomenon itself. Their own ego is also a factor – will a downround signal weakness? Anxiety slowly crept into everyone’s world.

Startup Founders: Don’t Forget to Sell the Dream | by Jason Shen – [link]. The Damaging Psychology of DownRounds | by Mark Suster – [link]. Hospital Prices No Longer Secret As New Data Reveals Bewildering System, Staggering Cost Differences – [link]. “Embrace skeptics. ” [link]. .”

While many travel industry leaders chose to “go dark,” as Airbnb CEO and co-founder Brian Chesky put it , while they decided how to navigate next steps, Chesky took a different approach: He got candid. Today, we are thrilled to have Airbnb CEO and co-founder Brian Chesky with us. We’ve kind of designed the kind of growth that we want.

And now I have to explain to team that they’re taking more dilution than they expected if we do a downround. A downround? I know how to structure around that to protect the founders from getting screwed on a multiple liquidation preference. There are a million ways to do quick, easy, low-costrounds with prices.

Some businesses require very little capital and the founder can self-finance the enterprise and retain 100% of its ownership and control from ignition through liquidity event (startup through sale). And even with the significant cost of credit card debt, many entrepreneurs aggressively use existing cards to finance a startup.

While many travel industry leaders chose to “go dark,” as Airbnb CEO and co-founder Brian Chesky put it , while they decided how to navigate next steps, Chesky took a different approach: He got candid. Today, we are thrilled to have Airbnb CEO and co-founder Brian Chesky with us. We’ve kind of designed the kind of growth that we want.

61% of VCs said valuations were “marginally down” in Q4 of 2015 but 91% expect price decreases in the next two quarters. In fact, 62% of VCs surveyed – across a wide variety of stages and geographies – said their portfolios were starting to cut costs, expected the markets to tighten. Most flat rounds.

Some businesses require very little capital and the founder can self-finance the enterprise and retain 100% of its ownership and control from ignition through liquidity event (startup through sale). And even with the significant cost of credit card debt, many entrepreneurs aggressively use existing cards to finance a startup.

Some businesses require very little capital and the founder is able to self-finance the enterprise and retain 100% of its ownership and control from ignition through liquidity event (startup through sale). And even with the significant cost of credit card debt, many entrepreneurs aggressively use existing cards to finance a startup.

I can switch to SaaS for less than the cost of the maintenance on the old software.” Alexia Tsotsis: Are you seeing downrounds because the NASDAQ is down? Marc Andreessen: No, we have not seen downrounds yet. I have got to make this stuff work on iPhones anyway, so I have got to do something new.”. “My

This is only a minor problem in that both forms can convert easily into ‘C’ corporations at low cost and little consequence. Second, it is important in the first investment round to face the issues that may be required later by subsequent, more sophisticated, investors such as VC’s.

Cendana founder Michael Kim was amongst the earliest and certainly the most focused LP to spot the changes in venture capital leading to seed stage funds and has backed many of the best in the industry so it’s always a pleasure to come and share thoughts with all of these great peers. 25% “downrounds?

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content