This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you track the venture capital industry it would be hard to miss the conversation going on this week over AngelList “Syndicates.” My favorite new VC blogger, Hunter Walk, weighed in with some thoughtful comments about how Syndicates might actually pit, “ angel vs. angel.” Must be doing something right!

Similarly, the best kind of dealflow for a VC is organic dealflow. Even if you are just meeting a founder for the first time, I think of dealflow as being organic when an intro is made by a founder that the investor trusts well before an active fundraise process has begun.

Syndicates Those in charge of a syndicate are called “syndicate leads.” Individuals invest modest sums in numerous businesses, even when working together in syndicates such as angel networks. The earliest investors in a business are usually syndication.

We are also seeing more investors try to be a part of syndicated A rounds for companies that are raising $5M or more and are really not what most would consider “seed” stage. Great returns in early stage investing is driven by great dealflow and good picking. This is not what Nextview is about.

We recently funded Blinkfire Analytics using our FG Angels Syndicate. So, we were psyched he was willing to do an FG Angels Syndicate with us. When it was oversubscribed they kept their syndicate commitment, but offered a much bigger investment outside the syndicate. I asked him if I could post them – he said yes.

Take a look at the founding syndicates of each: Masstor Sytems (5/1979). Quantum Corporation (6/1980). What is striking about these syndicates is that nobody had any meaningful capital, which forced syndication and cooperation. Some were Silicon Valley early stage companies, such as Apple, Quantum, and Masstor Systems.

For example, we created a pipeline management tool that automatically adds deals along with relevant information (such as attachments received) to our funnel. This tool serves to standardize & automate the process of collecting inbound dealflow. It seamlessly creates a deal folder (company name) in our Google Drive.

For example, we created a pipeline management tool that automatically adds deals along with relevant information (such as attachments received) to our funnel. This tool serves to standardize & automate the process of collecting inbound dealflow. It seamlessly creates a deal folder (company name) in our Google Drive.

Historically, seed rounds were syndicated among several different firms. These funds would regularly share dealflow with one another and could share the work in supporting founders and helping to push the company forward. Instead of broadly syndicated rounds, we are seeing much more competition for fewer slots.

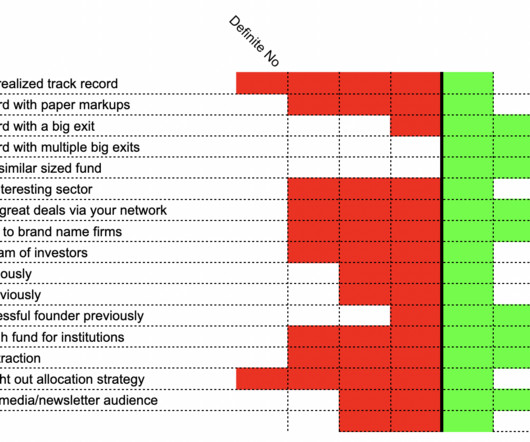

On the other hand, I feel things are a lot more predictable on the fund side—and that getting limited partners for your fund or syndicate is a lot more grounded in something that resembles logic. Yes, as track record is a combination of dealflow and deal selection. Are there proxies for track record?

Recently on this blog, I’ve been attempting to unpack how an investor can sort through dealflow and potential investment opportunities. After writing about “ the quick kill ” to discard of inbound flow, next I wrote about what actually captures my attention and graduates to a meeting.

She answered, ‘We see a lot of deals.’ I said we had a lot of dealflow. Chris Dixon, Partner, A16Z, observes , “Success in VC is probably 10% about picking, and 90% about sourcing the right deals and having entrepreneurs choose your firm as a partner”. Kushim manages your dealflow and track portfolio performance.

If you’ve been following along at home, you know that we recently created an AngelList Syndicate called FG Angels. We’ll contribute $50k to each investment; our FG Angels Syndicate will contribute up to $450k. 2 angels are considering creating their own AngelList syndicate as a result of their experience.

We are also seeing more investors try to be a part of syndicated A rounds for companies that are raising $5M or more and are really not what most would consider “seed” stage. Great returns in early stage investing is driven by great dealflow and good picking. This is not what Nextview is about.

Micro VCs are notorious for building large and friendly syndicates. While traditional VCs sometimes have a love/hate relationship with their syndicate partners (often depending on how well their mutual portfolio companies are performing), it seems as though in the Micro VC arena all of the players speak and act like best friends.

Benefits of joining a group include pooling dealflow, capital, domain expertise, and investing experience. Most groups run regular education sessions for new members, and provide mentoring for less experienced investors by those with many deals under their belt.

Sebastian Soler recently launched Knowledge.vc , which uses software and machine learning to enhance deal sourcing and diligence for VC firms. 4) Manage dealflow. For example, we created a pipeline management tool that automatically adds deals along with relevant information (such as attachments received) to our funnel.

We describe Foundry Group ‘s behavior as “syndication agnostic.” Because we are syndication agnostic, we are delighted to work with great co-investors and welcome and encourage the interaction and partnership. ” When we make an investment, we are completely agnostic as to whether or not we have a co-investor.

Are investors allowed to come into deals that the fund does side by side with the fund? This creates a source of dealflow for investors who aren’t out there full time creating opportunities. In fact, those deals are actually set up as mini-funds. Access to the partner.

Either they build a firm in order to outsource the screening and sourcing, they don't do as much deal leading, choosing to follow instead, or they go later stage to narrow their aperture to a much smaller set of companies that already have traction and shrink the amount of dealflow they need to look at.

Dealflow, then, is often a random walk. Slowly I have learned – the association investors have with certain founders, syndicate partners, and downstream VC firms matters; the people one chooses to work with as investor matters a great deal; and while the decisions may happen quickly, they stick around for a long time.

After two years of a dedicated experiment, we’ve decided to stop making new investments via our FG Angels Syndicate. The Monday after AngelList announced their Syndicate product in September 2013 we decided to to jump in with both feet and start FG Angels. Average syndicate investment amount per deal: $316k.

Those employees and operators, who often have some book wealth now (or are running syndicates on AngelList or acting as a scout for another fund) can easily dump $50K-$100K into one of their ex-colleague’s new startups, or put this money into their friend’s new startup, or their friend’s new hot deal.

This matching structure takes advantage of the industry knowledge, proprietary dealflow, and network of senior executives. – If an employee wants to invest at least $25K in a private company, she can nominate it to the Syndicate VC (“SVC”). Trevor Bond , former CEO of CEO of W.P.

Mechanics Angel investors often syndicatedeals, which means they join togetherto invest on the same terms. In a syndicate there is usually a"lead" investor who negotiates the terms with the startup. Dont feel like you have to join a syndicate, though. This isyet another problem that gets solved for you by syndicates.

We try to maintain a pretty steady investment pace each year, although it tends to ebb and flow a little bit based on our dealflow and valuations in the market. Syndicate diversification. So for the most part, we try not to be too dogmatic about syndicate partners.

Find out what the buzz is all about and make valuable connections with local investors who you can syndicatedeals with. You should come along for the ride if you are interested in investing more in Texas technology and disruptive commerce companies and want to develop relationships with local investors who can be your dealflow.

It was a great product addressing a large market opportunity and was interested in seeing how the AngelList syndicate process worked. Due to confidentiality provisions, I can''t disclose details, but there are many very unhappy participants who invested through the syndicate. Syndicates can either be company led or investor led.

I syndicated (helped them put together the round) in five: Notehall, MyZamana, Locately, Zippykid, and Instinct. Get an edge (lower valuations, better dealflow, etc.) Here are the basic stats: We've made eight initial investments and one follow-on. by leading rounds and being willing to jump first.

We have such a deluge of inbound dealflow via our network that we are not investing a lot of energy seeking out additional companies to filter. That said, our experience so far is that these online markets are most useful to identify opportunities to join a syndicate, not to source and lead a new investment.

The firm attracts dealflow by promising a decision (positive or negative) in under 2 weeks, with minimal paperwork and without repeating due diligence. Coinvestors need to figure out ways to prioritize themselves in a VC’s preference stack for syndicating opportunities.

Gust (the company I founded) is the online platform used by over 45,000 accredited angel investors and VCs, from over 1,000 angel groups and venture funds, in 74 countries, to manage their startup deals.

Gust (the company I founded) is the online platform used by over 45,000 accredited angel investors and VCs, from over 1,000 angel groups and venture funds, in 74 countries, to manage their startup deals.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content