This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Other founders, “as a privately held company we don’t disclose our valuation.&# Me, “dude, I’m not a journalist. I just want to figure out what a fair valuation is.&# I figured all the VC’s talked so we should. This starts with understanding how VCs and entrepreneurs often see valuation differently.

Investors may not be called co-founders, but they always get equity, commensurate with their share of the total costs anticipated, or share of the current valuation. Of course, all co-founders need to remember that allocated percentages will be diluted as angel and VC investors are brought in. Amount of venture funding provided.

If the company's valuation is $2 million, $90k is 4.5%. Of course, to be able to use this kind of formula, you will need to be able to determine how much impact the person will have and figure out a valuation. I've talked about this topic before in How Investors Think About Valuation of Pre-Revenue Startups.

We drew this conclusion after a meeting we had with Morgan Stanley where they showed us historical 15 & 20 year valuation trends and we all discussed what we thought this meant. But rest assured valuations get reset. When you look at how much median valuations were driven up in the past 5 years alone it’s bananas.

This is the first of a six part series on different methods used by angel investors to arrive at pre-money startup valuations. It is one of the most useful methods for establishing the pre-money valuation of pre-revenue startup ventures. Return on Investment (ROI) = Terminal (or Harvest) Value ÷ Post-money Valuation. (in

We recently started a series of posts on establishing the pre-money valuation of pre-revenue startup companies for purposes of investment by seed and startup investors. It is one of the useful methods for establishing the pre-money valuation of pre-revenue startup ventures. Post-money Valuation = $ 2.125 million. million ÷ 20X.

What the entrepreneurs were really saying is, “I don’t want to take a lower valuation now, while I don’t have customers or a full team. In a standard VC term sheet there is a standard term called an “anti dilution provision” and they are in nearly 100% of deals. ” Full R at-shits.

2: As expected at least one person accused me of writing this post because I want to see lower valuations. As the risks below get eliminated the higher the valuation investors are prepared to pay. So rounds tend to be “range bound&# where the top end of the valuation spectrum often being done in boom markets (i.e.

Investors may not be called co-founders, but they always get equity, commensurate with their share of the total costs anticipated, or share of the current valuation. Of course, all co-founders need to remember that allocated percentages will be diluted as angel and venture capital investors are brought in.

Investors may not be called cofounders, but they always get equity, commensurate with their share of the total costs anticipated, or share of the current valuation. Of course, all cofounders need to remember that allocated percentages will be diluted as angel and VC investors are brought in. Amount of venture funding provided.

Hire when it feels like you're bursting at the seems or missing a critical skill on existing team or have figured out how to scale growth — @msuster 6/ Raising capital at very high prices helps avoid short-term dilution. But if you raise at too high a price you make it harder to raise next round.

Investors may not be called co-founders, but they always get equity, commensurate with their share of the total costs anticipated, or share of the current valuation. Of course, all co-founders need to remember that allocated percentages will be diluted as angel and VC investors are brought in. Amount of venture funding provided.

Either would be fine with startups, so long as they can easily change their valuation. The key is making sure the second close isn’t too high (I think 50% of X sounds about right) because you’ll be adding on that dilution to yourself & “X&# investors will own less of the company. I agree on all points.

The challenge with pre-seed rounds is that pricing will sometimes be pretty dilutive. The downside is that YC is itself quite dilutive, the program itself may not be a great fit, and there are many many companies out of your batch that won’t be one of the anointed winners. The Pre-YC Pre-Seed.

They should heed the age old advice that raising slightly more money while you can is always better than trying to optimize future valuations. Should VC’s really be impacted by public market valuations when the money that they’re investing today should be for returns in 7-10 years? Short answer – yes.

million pre-money valuation, which is a $10 million post-money) you get diluted by 25% (2.5m / 10m). But understanding how you’re likely to get diluted over time is a more difficult concept. So here is our crack at explaining the world of dilution to you. This post originally appeared on TechCrunch. million at a $7.5

Everyone moved to earlier stage – part of the decline in late stage investing is the ‘baggage’ of companies that previously raised money at inflated valuations that they would struggle to justify in today’s market. That’s yet another reason for micro funds to move earlier in the fundraising timeline.

It also is a great way to finance your business without facing dilution before you actually raise venture capital and when the valuation you might get from angels is less than you’d want. So it wouldn’t bother me if 90% of your year-one revenue was PS provided it was done with a specific plan for year-2 software sales.

Every time a startup raises capital, all common shareholders are diluted. As an aside for founders, there is an interesting approach on how to arrive at equity offers outlined by Fred Wilson that may be worth checking out once there is a sense of valuation. All of the estimates displayed above are figures prior to any dilution.

This has a tangible impact on the valuation of start-ups and the pace of investment. If you’re raising $2 million and can close on $3 million – don’t optimize to minimize short-term dilution, optimize for contingencies in case the market gets worse. Bad stock markets mean less IPO’s and lower prices for M&A.

” If you invested at $8m pre-money and put $2m in (thus you own 20% of a company at a $10m post-money valuation) and if you put another $2m into a round at a $40m valuation raising $10m ($50m post) you end up with half your money at $8m pre and half at $40m pre thus your average price goes up dramatically. That seems fair.

One of the challenges for investing in startups has always been the lack of an established way for founders and investors to actually measure and decide on the valuation of the startup concerned. ” Ideaspotting investment pre-money valuationvaluation Worthworm'

The startup industry may be “resetting,” which doesn’t mean a “crash” but rather just a resetting of valuations, timescales, winners/losers, capital sources and the relative emphasis of growth rates vs. burn rates. Optimize for a W more than % dilution in these circumstances. Be realistic on valuation.

The key to this strategy is getting 5 people who form the social proof to help you get a bigger angel round done at a higher valuation by tons of industry insiders and thus offering the social proof you need attract great employees and ultimately venture capital investors.

@altgate Startups, Venture Capital & Everything In Between Skip to content Home Furqan Nazeeri (fn@altgate.com) ← No one wants to tell you your baby is ugly More on Liquidation Preferences → Pre-Money Valuation vs Number of Founders Posted on December 15, 2010 by admin Here’s a chart of the day worth sharing.

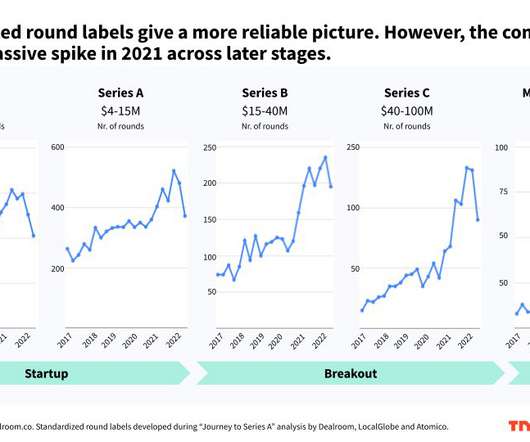

According to new research by Pitchbook , the trickle down effect has already started in seed and series A startups with round sizes and valuations shrinking in size compared to 2021. But recently those round sizes and valuations have tumbled to about $10 million and $50 million, respectively, he said. Lemkin #????????????

Investors may not be called co-founders, but they always get equity, commensurate with their share of the total costs anticipated, or share of the current valuation. Of course, all co-founders need to remember that allocated percentages will be diluted as Angel and VC investors are brought in. Amount of venture funding provided.

Term-sheets and Valuations: Thinking about Negotiations. I’ve sat down with entrepreneurs and a copy of a term sheet guide I like [ “Term Sheets & Valuations - A Line by Line Look at the Intricacies of Venture Capital Term Sheets & Valuations ” by Alex Wilmerding, Aspatore Press.] The Valuation Question.

Over the last 10 years, we’ve been in a bull market with considerable froth in late stage financing activity and valuations. The cases of WeWork and Uber cast a cloud of doubt over funds that are largely driven by one or two outlier companies that may have a tremendous valuation, but shaky underlying business metrics.

I thought I’d write a post about how to talk about valuation at a startup and give you some sense of what might be on the mind of the person considering funding you. It’s not uncommon for a VC to ask you how much capital you’ve raised and what the post-money valuation was on your last round. is to start with just the data.

The equity dilution at this nascent stage is on desirable terms; such investing can lead to profitable returns. Here, the company’s valuation benchmark is set, and funding is solicited accordingly. 2) Seed funding. Promoters try to raise this funding majorly from Angel Investors. 3) Series A, B, C funding.

The bridge or exit stage is generally of very large transactions and for companies with substantial valuation. The essential components of your pitch include a comprehensive business plan with projections of 5 years along with investment offerings and estimated valuations. Point number 3: Never raise money with an increased valuation.

Not to mention the fact that every time you compensate with equity, you dilute your own ownership of the business. Any decision to hand out stock or stock options should be made within the big picture context of your company’s valuation and the total number of shares you’ll be granting. Tips for compensating with equity. Plan upfront.

Executives run the day-to-day so often the board is more involved as a sparring partner at key intervals. The administrative work we actually do at board meetings? Boards are not appointed to be founder-friendly lapdogs for the 1–3 founders who start companies and usually own the largest equity positions in the company.

So, let’s say that one founder puts in $100,000 in seed capital, that could be worth 20 percent of a seed stage company’s valuation. So, a fair split, would be closer to 60/40 in favor of the funding founder, when diluted for the cash.

Raise too soon and likely take on more dilution, wait and get valuation up (as our metrics continue to rise) but then run to a point where you have a lower cash balance and place more risks on the business. These are the hard problems we’ll have to address in the year ahead along with the perennial, “ When should we raise more money?

What’s critical for entrepreneurs to understand is that valuations for startups do not increase at a linear rate; they increase geometrically based on achieving the right milestones. The best entrepreneurs raise enough money to achieve a set of interim milestones and then raise capital again at a significantly increased valuation.

Many Asian entrepreneurs tell me that they want to raise funds from Silicon Valley firms because they perceive the valuations to be higher. Valuations are based more on typical later-stage type of metrics. Finally, don’t over-optimize on valuation. Third, investors are generally much more conservative in Asia.

When times are really good for fund raising many teams delay to maximize their valuation. If you are able to raise money from credible sources at a reasonable dilution percentage then I personally favor getting the round done now and building your business. How much dilution am I going to have to take now? 25% dilution).

Not only can valuations rapidly outstrip fundamentals and become artificially high really fast, they’re also deceptively stable. This makes sense at face value: a) fundraising ranges from being a distraction to a colonoscopy + root canal, b) dilution sucks, and c) they are quantifiable attributes, easy to compare or rate good/bad.

Third (if you’re keeping score), it is not wise to dilute the founder’s ownership greatly in the first round of financing. Giving control over that vision to others early on often dilutes the vision and is a disincentive to the entrepreneur. Email readers, continue here…] Fourth, there is the matter of control.

You can get cash without diluting your ownership in the company. Why not go further, develop more valuation, customer experience, and really, deeply validate the business? In 1M/1M, our preferred financing strategy is customers. Because customer financing equals revenue, not equity.

Should founders have anti-dilution rights? You would want to check and see if your shares can be diluted. Yes, you could be diluted from 10% down to 1% and there’s a number of reason why that could occur. Dilution should occur across the board. What is the equity I should expect (protected from dilution)?

Never, ever, choose your investors based on valuation. A couple of dilution points here or there wont matter in the long run but working with the right people will.? Alignment of business objectives and personal relationships means tons more than valuation. Don’t skimp on fundraising because of dilution fears.?.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content