This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The top quartile has distributed 2.03x (vs. 1.68) and the median fund now has distributed 1.27X (vs. The longer the portfolio maintains the same value without distributing back cash, the worse the fund’s ultimate IRR. Based on that metric, the top quartile fund has now distributed 2.03X after 12 years. 2 years ago).

At the Upfront Summit in early February, we had a chance to have many off-the-record conversations with LimitedPartners (LPs) who fund Venture Capital (VC) funds about their views of the market. However, they have been sending VCs far more investment checks in the last ten years than they’ve gotten back as distributions.

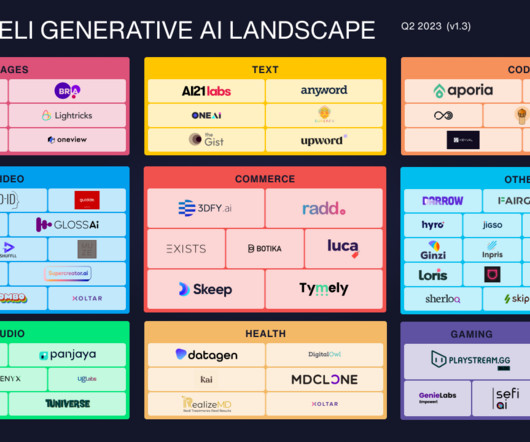

Several of our limitedpartners are media and entertainment strategics: broadcasters, publishers, telcos etc, so content creation, distribution and monetisation has always been close to our core focus. At Remagine Ventures we started investing in the generative AI space very early back in 2019.

” A second point of clarity is often the secondary is being performed for reasons other than just distributions to LPs, but also helps the venture firm recycle capital to support other startups in the firm’s portfolio. As an industry peer said to me, “I think friendly secondaries are easy, everything else feels new.”

– I spoke about GRP’s recent exit of Ulta in which we returned $320 million to our limitedpartners. Can you please expand on your post about distributed teams? It was a verbal discussion on my post on distributed teams. - Yes, that was the value that we actually returned as opposed to the value of Ulta.

A more efficient approach to fundraising than haphazard networking is to mine the data exhaust from the limitedpartner universe to identify those LPs most likely to find your fund attractive, and focus all your energy on them. Cobalt for General Partners helps GPs to optimize their fundraising strategy. 11) Exit .

They’re taking a $1m check from me, or giving $5m to me as a limitedpartner. Other coinvestors: Limitedpartners, other VCs who are coinvestors, private equity funds which are potential growth-stage investors, etc. Distributing content. But for B2B sales, meeting people in person is often mandatory.

For example, our limitedpartners have major ownership interests in such companies as Adidas , LafargeHolcim (largest building materials manufacturer in the world), and SuperNAP International (developer of data center facilities worldwide; used by Amazon, Intel and Microsoft).

Yes, VC / Startup Funding is up Massively If you look at how much VC firms have raised from LimitedPartners (LPs) over the past 2 decades you’ll see that we’ve returned to a level that we haven’t seen since 1999. If you want the whole deck you can find it on SlideShare but I’ve written up a short summary with commentary below.

Similar to the explosion of seed funds in the past decade, we (and some limitedpartners too ) believe these Flexible VCs are on the forefront of what will become a major segment of the venture ecosystem. Flexible VC creates early liquidity which can be either reinvested or distributed to LPs. Early liquidity.

No distributed teams, no overseas teams, and definitely no companies that rely on “outsourcing” to build their core technology. This new $40M fund is backed by several high quality institutional limitedpartners including university endowments, foundations, family offices and fund of funds and key individuals.

No distributed teams, no overseas teams, and definitely no companies that rely on “outsourcing” to build their core technology. This new $40M fund is backed by several high quality institutional limitedpartners including university endowments, foundations, family offices and fund of funds and key individuals.

Ramanan Raghavendran, Managing Partner at Amasia , explains how they’re managing their processes: “At Amasia, our distributed presence on both sides of the Pacific mandates the use of technology to be effective, timely and coordinated. How do funds use tech to monitor and report investments?

From who we hire to the way we go to market, from how we engage with our limitedpartners to how we engage with founders, it’s all about being very focused on quality and consistency so as to affect strategies to generate meaningful carry for ourselves and our limitedpartners.

Venture capital funds are usually 7 - 10 year partnerships whereby the general partners - the “VC” - manage the capital of the limitedpartners, usually institutions (endowments, pension funds, etc.). At the end of the period, all profits and proceeds are distributed to the various partners on a pre-determined split.

As a former institutional investor, one of the stats we focused on was carry distribution. Very few institutional LimitedPartners have reached out to their investors to even ask about VC policy, let along try to influence it. Morever, LPs should be influencing these policies.

If our dev shop had shareholders expecting a profit, or if I personally took distributions from it, it would be dangerously tempting to overpay for development services. The success of the dev shop would be in constant conflict with capital efficiency within the portfolio.

If our dev shop had shareholders expecting a profit, or if I personally took distributions from it, it would be dangerously tempting to overpay for development services. The success of the dev shop would be in constant conflict with capital efficiency within the portfolio.

We recently shared three key trends with our limitedpartners during our Annual General Meeting. The COVID-19 pandemic led to the rise of remote and distributed teams, a trend that continues today as companies seek cost savings and access to global talent. By the time we reached Fund III, the dynamics shifted.

Cambridge Associates is a service provider to the LimitedPartners that invest in venture capital funds that’s known for the quality of its research. Their advice to LPs is to catch these distributed returns by investing in emerging managers outside of traditional US venture heartlands.

Who wouldn’t accept an invite to “A networking breakfast where 7 midstage startups will be able to give short demos to the CEO/COO/Head of Business Development/etc for Big Interesting Company X that has huge reach/distribution/userbase, etc.” Maybe make it sector focused and bring in a bunch of such contacts.

On #2, we have been fortunate to collaborate with a wide group of exceptional entrepreneurs, coinvestors, and limitedpartners. Just like any other startup, the question we are focused on post series A is whether we are doing the right things to allow us to win in a competitive market with a power-law outcome distribution.

We don’t normally distribute literature at these events, but we do prepare FAQs beforehand (not for distribution) to make sure that we’re all aligned on our talking points. We currently participate in events as speakers and plan to continue hosting periodic events to build awareness around our fund and portfolio companies.

No distributed teams, and no outsourced product development. I would like to take a moment to thank K9′s LimitedPartners for their support of this first fund. Capital Efficient : Companies that need a Seed round, probably a Series A, but potentially may not need a Series B or Series C.

Now Fortune has obtained more granular data, including returns for dotcom-era funds managed by such firms as Accel Partners, Benchmark Capital, General Catalyst Partners and Lightspeed Venture Partners. Through 12/31/11, less than 66% of the fund-of-funds called capital had been returned to limitedpartners.

San Antonio has Geekdom with USAA and Port San Antonio with the Air Force Cyber Command; Houston has The Ion with Rice University, Microsoft and NASA and The Cannon distributed across the city; Dallas has Pegasus Park with UT Southwestern and Lyda Hill Philanthropies; and Austin has Capital Factory with the Army Futures Command.

If you were a “with it” VC you needed to have a “Content&# or “Multimedia&# company in your portfolio to impress your limitedpartners – educational software companies, game companies, or anything that could be described as content and/or Multimedia. We understood none of this. More detail in future posts.

I was a LimitedPartner in Angel Investors II (Ron Conway's angel fund) that was an investor in Confinity. Luckily, Google was one of the 150 and did ultimately return the fund assuming the LP was smart enough to hold the stock after distribution. At the IPO, Musk held a 14.2% stake vs Thiel's 5.6% (Sequoia Capital had 10.7%).

I’ll also continue to work within the NYC tech community—now thriving at a level I could hardly have imagined when I first got the pitch deck for USV’s first fund as a LimitedPartner at the GM pension fund. To think, I almost didn’t take that 2004 meeting because it was a NYC-based fund.

When you''re out on the road pitching, and getting people to believe in you, you feel a deep sense of responsibility to your limitedpartners--and there isn''t a day when you don''t wonder why you didn''t just take some easy corporate job where no one would notice if you weren''t working productively.

All Unicorn participants — founders, company employees, venture investors and their limitedpartners (LPs) — are seeing their fortunes put at risk from the very nature of the Unicorn phenomenon itself. LIMITEDPARTNERS (LPS). They are the real capital that make the system work.

While the M&A story has been widely reported perhaps far fewer people know that LimitedPartners (LPs), the people who fund VC firms, have finally been able to restock their coffers in the past 4 years with significantly more money coming to them in distributions than capital calls to fund VC firm investments.

Ampex’s first customer was Bing Crosby who wanted to record his radio programs for rebroadcast (and had exclusive distribution rights.) million of it by the time they dissolved their partnership in 1968 – they returned $90 million to their limitedpartners – a 54% compound growth rate.

Distributions can actually be drawn out over an extended period of time, but for the purposes of this exercise, I just kept the fund to 11 years. Do seed investors have LimitedPartners with different return expectations than Series A and beyond investors? It's what you'd expect. That's if you're not following on.

One of the folks, Lisa Cawley (Screendoors Managing Director), recently published a blog post called Work with your LPAC, not for your LPAC , which got me thinking about Homebrews LPAC (LimitedPartner Advisory Committee).

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content