This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It’s a tough time for a lot of startup founders right now. Many companies are now having to resort to tough measures in order to stay afloat, including layoffs, downrounds and tough terms from current investors. What is a founder to do? If the answer is yes, then a downround is likely the best path forward.

The past year was a wild ride for startups and founders, giving a whole new meaning to the ”rollercoaster” aspect of being an entrepreneur. Patrick Collison , self-made billionaire founder of Stripe. Bill Gates , founder of Microsoft. A good way to think about valuation in seed/pre-seed is to reverse engineer the next round.

” In the article I discussed the downside of raising capital at a too high of a price and referred people to a previous article I had written encouraging founders to raise “ At the Top end of Normal ” as opposed to stratospheric prices. The Damaging Psychology of DownRounds. A downround.

Amongst the most often asked questions I get from founders is, “How much money should I raise?” Reflexively founders want to raise as much money as they can because they figure it will give them more resources, better chances of competing and a longer runways before they have to do the often painful job of asking, yet again, for money.

The A round was done in February 2000 (end of the bull market) and my B round was done in April 2001 (bear market). As a result I had to do a downround. Downrounds are psychologically really difficult on companies and can make it harder to do later rounds. I eventually needed more money.

I’ve decided to take all of my private conversations and subjective points-of-view on the topic and make them public in a keynote speech at the Founder Showcase in San Francisco on June 15th. Finally, even if they could bring themselves to offer you a major downround, the more sophisticated investors know it’s fool’s gold.

by Michael Woolf that is worth any startup founder reading to get a sense of perspective on the reality warp that is startup world during a frothy market such as 1997-1999, 2005-2007 or 2012-2014. Burn rate in case you don’t know is the amount of money a company is either spending (gross) or losing (net) per month. (it

I recently spoke at the Founder Showcase at the request of Adeo Ressi. I said that at the Founder Showcase, too. And for many of these they were (over) funded 7-10 years ago and don’t necessarily all represent great returns for investors or founders. New investors hate downrounds. That’s a fact.

A founder asked me what makes a $2M round “pre-seed”? And why do we still sometimes hear about pre-seed rounds that look more like a series A in pricing and size? What’s the difference between an angel round and pre-seed round and why do I believe we’ll see more pre-seed rounds taking place in 2024?

Most founders reported (in several different surveys) that knowledge and belief in their industry/sector and personal connection is one of the key reasons they would choose one investor over another. See the recent reports by Frontline Ventures and Creandum on what makes founders choose one offer over another.

In times when venture capital is hard to get, investors extract high costs for failure (down-rounds, cram downs , new management teams, shut down the company.)

Most existing investors (those still in business) hoarded their money and stopped doing follow-on rounds until the rubble had cleared. Except, that is, for the bottom feeders of the Venture Capital business – investors who “ cram down ” their companies. A cram down is different than a downround. You Have a Choice.

She has a good article today in TechCrunch titled Embrace the downround (it’s going to be okay, maybe). ” Now, I’m not encouraging anyone to do a downround if unnecessary., ” Now, I’m not encouraging anyone to do a downround if unnecessary.,

Don’t assume that you can “just do a downround” if necessary. Downrounds are corrosive. Founders hate them because they’re dilutive. Insiders hate them and fight them. Outsiders hate them because they are worried about p **g off your existing investors.

The founders were very sympathetic; a man, laid off from his job, and his very pregnant wife, who sold their house and investing $150k into the business and are working hard to make a go of it. The two founders invested $40k in the business, and plan to license it rather than manufacture it because manufacturing seems too hard.

But recently those round sizes and valuations have tumbled to about $10 million and $50 million, respectively, he said. As a result, founders are accepting increased dilution of the stakes they hold in their own companies. With over 1,000 global unicorns (and about 1.5 As an example, here are 34 new unicorns minted in May 2022.

It is not a strong bargaining position for the CEO to ask for money to complete a product promised for completion with the previous round of funding. And professional investors often penalize the company with lower-priced downrounds or expensive loans as a result.

I have interacted with a lot of founders who funded their initial business expenses through credit cards. Point number 1: You must understand that funding is a business transaction between the investors and the startup founders. But, in subsequent rounds of funding inflated valuation will be normalized resulting in a downround.

Plus, VCs often will have met the Founder/CEOs of many of a particular startup’s competitors, so they’ll have an even richer understand of the market landscape. Has there ever been a downround, inside round, a flat round, or a CEO change?

It is not a strong bargaining position for the CEO to ask for money to complete a product promised for completion with the previous round of funding. And professional investors often penalize the company with lower-priced downrounds or expensive loans as a result.

Type to Add and Search Questions; Search Topics and People Startups Startup Compensation Entrepreneurship Compensation Stock Options Major Internet Companies Silicon Valley Why is there such a large founder to early employee equity drop-off? The real question here is: why is it fair for founders to get so much more?

And now I have to explain to team that they’re taking more dilution than they expected if we do a downround. A downround? I know how to structure around that to protect the founders from getting screwed on a multiple liquidation preference. Raising lower seems kind of like something is wrong.

I have two simple rules for founders in my head from this experience. Then, if you end up doing a downround, it suddenly matters a lot. Don’t worry about this too much, until you do a downround. Then use the downround to clean up your preference overhang.

A typical startup goes throughseveral rounds of funding, and at each round you want to take justenough money to reach the speed where you can shift into the nextgear. I think it would help founders to understand funding better—notjust the mechanics of it, but what investors are thinking. Few startups get it quite right.

Startup Founders: Don’t Forget to Sell the Dream | by Jason Shen – [link]. The Damaging Psychology of DownRounds | by Mark Suster – [link]. The Start-up Hall of Shame (America’s 10 Worst States for Entrepreneurs) – [link]. Startups: You Should Value Software More | by Wade Foster – [link].

What was the post money on your last round (and how much capital have you raised)? It’s not uncommon for a VC to ask you how much capital you’ve raised and what the post-money valuation was on your last round. VCs hate “downrounds” and many don’t even like “flat rounds.” There are some simple reasons. After all?—?we

And people like Jeff Clavier, Aydin Senkut, Dave McClure, Chris Sacca & Eric Paley (at Founder Collective) are leading the charge. Chris Sacca talked about how a $20 million exit can change a founder’s life and that shouldn’t be scoffed at. That’s awesome. I had two kids and a rental house.

In VC: I see a fair number of deals that have reached some point of stagnation that are seeking a flat or downround. Every good founder I know writes a list of names when they are starting to prepare for fundraising. “The most important thing to do if you find yourself in a hole is to stop digging.” . This is bad.

The first capital a young company receives usually takes the form of common stock, the same class of shares the founders hold. Venture capitalists and later round investors like the preferred convertible shares. These “IV drip” financings may reduce risk for investors, but put more pressure on founders. Anti-dilution protection.

The first capital a young company receives usually takes the form of common stock, the same class of shares the founders hold. Venture capitalists and later round investors like the preferred convertible shares. These “IV drip” financings may reduce risk for investors, but put more pressure on founders. Anti-dilution protection.

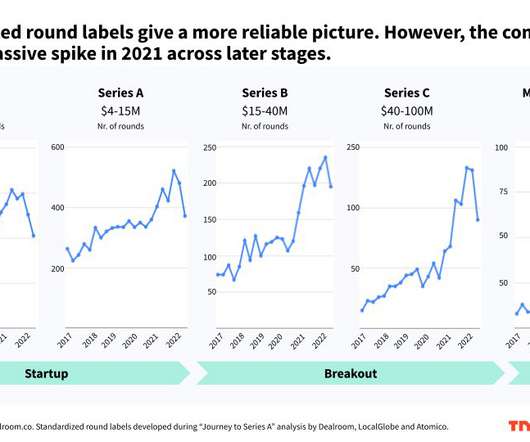

As Fred Wilson put in in his post ‘What will happen in 2023’ “I believe that ‘new normal’ is more or less where we were in 2015 where seed rounds were done around $10mm, A rounds were done around $15mm to $25mm, B rounds were done around $25mm to $50mm, and growth rounds had a cap at 10x revenues.”

This is a guest post from Rob May , a co-founder and CEO of Backupify , which raised $19.5M Hang out with other founders and CEOs. Other CEOs are the only people you can sit down and talk with about the hardest parts of your job. and sold to Datto in late 2014. Disclosure: NextView was not an investor in Backupify.).

All Unicorn participants — founders, company employees, venture investors and their limited partners (LPs) — are seeing their fortunes put at risk from the very nature of the Unicorn phenomenon itself. Their own ego is also a factor – will a downround signal weakness?

Founders Institute Plain Preferred Term Sheet (by WSGR – disclaimer, I represent the Founders Institute and was involved in drafting this document). Yes for Series Seed holders and founders. Y Combinator Series AA Equity Financing Documents (by WSGR). Series Seed Financing Documents (by Fenwick & West). Drag-along.

The first capital a young company receives usually takes the form of common stock, the same class of shares the founders hold. Venture capitalists and later round investors like the preferred convertible shares. These “IV drip” financings may reduce risk for investors, but put more pressure on founders. Anti-dilution protection.

Why Inside Rounds are Difficult? Many founders don’t understand why inside rounds are so difficult. Why DownRounds are Harder Than You May Think. Downrounds are hard. A slight downround is achievable but massive “hair cuts” are very hard to do.

And now I have to explain to team that they’re taking more dilution than they expected if we do a downround. A downround? I know how to structure around that to protect the founders from getting screwed on a multiple liquidation preference. There are a million ways to do quick, easy, low-cost rounds with prices.

It’s worth mentioning that the actual number is likely much higher, as rounds get reported long after they actually happened and September already started off with a bang. OpenAI co-founder and former CTO, Ilya Sutskever and his new SSI Inc. billion compared to $6.7 billion in Q1-Q2-Q3/2023. AI and all the rest. 35% of U.S.

While many travel industry leaders chose to “go dark,” as Airbnb CEO and co-founder Brian Chesky put it , while they decided how to navigate next steps, Chesky took a different approach: He got candid. Today, we are thrilled to have Airbnb CEO and co-founder Brian Chesky with us. BC: Yeah, Reid. And then we had actually raised money.

I always caution entrepreneurs not to take too high a valuation in any round because it sets very high expectations for the next round. A downround, which can damage a company and make it difficult to raise money in the future. Unfortunately, most startups don’t meet their initial rosy projections. What happens then?

When you go to fundraise, you will need to consider the possibility of a valuation lower than the valuation of your last round, i.e., the dreaded downround. Downrounds are bad and hit founders disproportionately hard, but they are not as bad as bankruptcy. Yes, we did a downround.

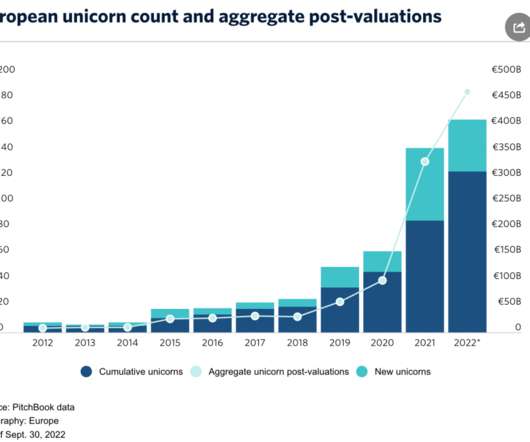

The 2022 Founders Factories report by DealRoom and Accel shines a spotlight on the startup clusters that produced most unicorns across Europe and Israel, and then tracks the alumni of those unicorns to test where the talent goes to found their next companies. London and Tel Aviv are home to the most founder nurturing unicorn startups.

Many startups extended runway, cut costs and took on painful downrounds or expensive debt to avoid raising in 2023. Rates coming down – The Fed is expected to cut interest rates this year, potentially thawing capital into startups, and opening up the IPO window (which will give funds/LPs liquidity).

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content