This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It’s a tough time for a lot of startupfounders right now. Many companies are now having to resort to tough measures in order to stay afloat, including layoffs, downrounds and tough terms from current investors. The pressure to protect portfolio startups seen as potential fund returners will be profound.

For those of you who have been following the discussion, a Lean Startup is Eric Ries ’s description of the intersection of Customer Development , Agile Development and if available, open platforms and open source. Over its lifetime a Lean Startup may spend less money than a traditional startup. Lets see why.

The past year was a wild ride for startups and founders, giving a whole new meaning to the ”rollercoaster” aspect of being an entrepreneur. A combination of competition for top talent and an effort to bring employees back to the office drove startups in Israel to throw extravagant parties and all-inclusive retreats abroad.

2 preamble issues having read the comments on TC today: 1: I know that the prices of startup companies is much great in Silicon Valley than in smaller towns / less tech focused areas in the US and the US prices higher than many foreign markets. That’s the deal you get when you’re raising in a good market for startup financing.

The A round was done in February 2000 (end of the bull market) and my B round was done in April 2001 (bear market). As a result I had to do a downround. Downrounds are psychologically really difficult on companies and can make it harder to do later rounds. I eventually needed more money.

I have often been asked about Startup Funding by entrepreneurs. Many myths surround the subject of startup funding. Here is Startup Funding, a Comprehensive Guide for Entrepreneurs. You must have seen a lot of startups giving out promotions, discounts, and incentives at the early phase of their business. Debt investors.

” In the article I discussed the downside of raising capital at a too high of a price and referred people to a previous article I had written encouraging founders to raise “ At the Top end of Normal ” as opposed to stratospheric prices. The Damaging Psychology of DownRounds. A downround.

Much has changed in the past four months of the technology startup world and how outsiders value the business. Don’t assume that you can “just do a downround” if necessary. Downrounds are corrosive. Founders hate them because they’re dilutive. Insiders hate them and fight them.

A founder asked me what makes a $2M round “pre-seed”? especially if the startup already has a product and revenue? And why do we still sometimes hear about pre-seed rounds that look more like a series A in pricing and size? Defining the pre-seed round It’s futile to look for ‘one true’ definition.

I recently spoke at the Founder Showcase at the request of Adeo Ressi. I said that at the Founder Showcase, too. And for many of these they were (over) funded 7-10 years ago and don’t necessarily all represent great returns for investors or founders. New investors hate downrounds. That’s a fact.

For the past 10 years, with interest rates near zero, VC investors plowed record amounts into tech startups and enjoyed a seemingly ‘easy’ investing environment. Prices went up from round to round, and startups were encouraged to grow, grow, grow, and not to worry about profitability.

Evaluating a startup as a prospective employee is tough, especially when you compare to VCs. Plus, VCs often will have met the Founder/CEOs of many of a particular startup’s competitors, so they’ll have an even richer understand of the market landscape. Is it shooting for a big market?

Cram downs are back – and I’m keeping a list. At the turn of the century after the dotcom crash, startup valuations plummeted, burn rates were unsustainable, and startups were quickly running out of cash. Except, that is, for the bottom feeders of the Venture Capital business – investors who “ cram down ” their companies.

The market correction has come for series A and seed startups. For the past few week I’ve been sharing here the impact of the current downturn that started in the public markets on startups and venture capital. Until now, early stage startups were relatively unaffected. It’s not just the prices that are coming down.

The founders were very sympathetic; a man, laid off from his job, and his very pregnant wife, who sold their house and investing $150k into the business and are working hard to make a go of it. The two founders invested $40k in the business, and plan to license it rather than manufacture it because manufacturing seems too hard.

Type to Add and Search Questions; Search Topics and People StartupsStartup Compensation Entrepreneurship Compensation Stock Options Major Internet Companies Silicon Valley Why is there such a large founder to early employee equity drop-off? Many startups these days are first-time entrepreneurs. is lowered.

Mark Suster wrote a great post yesterday titled The Resetting of the Startup Industry. I have two simple rules for founders in my head from this experience. Then, if you end up doing a downround, it suddenly matters a lot. Don’t worry about this too much, until you do a downround.

I thought I’d write a post about how to talk about valuation at a startup and give you some sense of what might be on the mind of the person considering funding you. Of course, unlike cars there is no direct comparison across each startup so these are just some general guidelines to try and even the information field.

by Rizwan Virk, author of “ Startup Myths and Models: What You Won’t Learn in Business School “. If you are building a startup, you’ll find no shortage of people who are willing to give you advice, particularly when it comes to raising financing. Unfortunately, most startups don’t meet their initial rosy projections.

Industry change allows the entry of newer players at earlier stages – It doesn’t take as much money to launch a startup anymore. So in the past we needed VC to really get a startup going. And people like Jeff Clavier, Aydin Senkut, Dave McClure, Chris Sacca & Eric Paley (at Founder Collective) are leading the charge.

The first capital a young company receives usually takes the form of common stock, the same class of shares the founders hold. Venture capitalists and later round investors like the preferred convertible shares. These “IV drip” financings may reduce risk for investors, but put more pressure on founders. Anti-dilution protection.

In VC: I see a fair number of deals that have reached some point of stagnation that are seeking a flat or downround. Every good founder I know writes a list of names when they are starting to prepare for fundraising. I haven’t seen many startup railroads. . This is bad. Tread very carefully. . And yet, Mr. .”

” “Mark has a vested interest in talking down valuations of startups.” Most prefer not to say this publicly for two reasons: 1) they have an entire portfolio of startups, many of whom are raising capital and 2) they prefer not to be attacked publicly or seem “anti entrepreneur.” goes into a startup.

A report by Greenfield Partners puts the total fundraising of Israeli startups at $15.16 Israeli startups 2022 funding summary. Downrounds, especially for growth stage companies, and bridge rounds galore. We started to see downrounds taking place especially in growth stage. billion to $17.1

The first capital a young company receives usually takes the form of common stock, the same class of shares the founders hold. Venture capitalists and later round investors like the preferred convertible shares. These “IV drip” financings may reduce risk for investors, but put more pressure on founders. Anti-dilution protection.

Founders Institute Plain Preferred Term Sheet (by WSGR – disclaimer, I represent the Founders Institute and was involved in drafting this document). Almost all startup companies don’t declare dividends, so deletion of a dividend preference is irrelevant to an investor. Yes for Series Seed holders and founders.

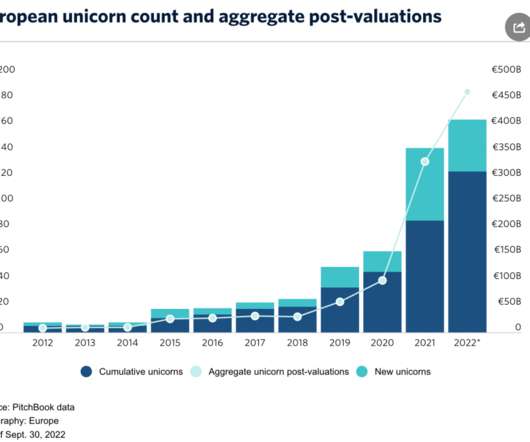

The 2022 Founders Factories report by DealRoom and Accel shines a spotlight on the startup clusters that produced most unicorns across Europe and Israel, and then tracks the alumni of those unicorns to test where the talent goes to found their next companies. London and Tel Aviv are home to the most founder nurturing unicorn startups.

No one can predict the future and it’s especially true in the startup world. The statistics show that even though most founders bet their time and resources that their startups will be the best in the world, 90% of those new startups won’t be in operation in 10-15 years. Key Variables to Consider: Sales units.

. “Many Unicorn founders and CEOs have never experienced a difficult fundraising environment — they have only known success. Also, they have a strong belief that any sign of weakness (such as a downround) will have a catastrophic impact on their culture, hiring process, and ability to retain employees.

We must #BRINGTHEMALLHOME August was a slow month in venture investment as globally startups raised $18 billion in August worldwide, a 37% decline MoM and 24% decline year over year. This was also felt in Israeli startups, who reportedly raised only $201M in 7 deals, bringing the total to $938 million in 61 deals in Q3 2024 so far.

2023 was a rough year for Venture Capital and for startups, and it might get even worse. I believe there are a lot of problems need solving, my outlook is longer term and I invest in new companies (most of the startups that Remagine Ventures II will invest in don’t yet exist). In many ways, Edward is right.

Usually unbeknownst to all, the decision around pursuing or accepting a venture capital round will be the most important factor in determining the investment return for the founder and the original angel investors in the company. But here is the key – contrary to popular wisdom it is negatively correlated.

I was reading Danielle Morrill’s blog post today on whether one’s “ Startup Burn Rate is Normal. I love how transparently Danielle lives her startup (& encourages other to join in) because it provides much needed transparency to other startups. ” I highly recommend reading it. Valuation.

I have written about startup valuations previously. If you are advising startupfounders, I strongly suggest having them read all 4 of the posts to get the lay of the startup valuation land. A founder is about to raise their first round and asking me how to value their company. [1]. Active users.

Amongst the most often asked questions I get from founders is, “How much money should I raise?” Reflexively founders want to raise as much money as they can because they figure it will give them more resources, better chances of competing and a longer runways before they have to do the often painful job of asking, yet again, for money.

Investors sat with the founder & CEO, Jason Spievak, and asked him what he wanted to do about the future. Investors had grown too used to the idea that any deal you funded would get marked up to a higher valuation in the next round and that’s clearly not always true. Some startups will have a hard time reorienting.

Our estimates were not out of line with new data from top firms like USV who, according to reports, “ marked down the value of seven of its funds by nearly 26%.” Restructures, DownRounds, and Pay to Plays. And fascinating new advances (and needs) in AI, climate, biology, etc are driving tech-IP driven startups.

The funding environment for tech startups is an ever shifting ground as we go through predictable shifts that go hand-in-hand with the slowing of the overall market. Boom in Number of Startups. There was an explosion in number of startups both because it was cheap and there was tons of available capital.

Startups everywhere will need to adjust their fundraising strategies and good investors will be helping them to adjust quickly – it’s much less painful that way. However severe our current situation is, I’m sure there will be plenty of short term negatives, including more job losses, company failures and downrounds.

Everyone loves a high valuation and it’s natural for founders to want to minimise dilution. They will most probably go on to raise multiple rounds of venture capital after all. YC’s Sam Altman explained why in a post last year: Startups are usually a pass-fail course — either you succeed or you don’t.

It is highly typical for a startup to have small investors on its cap table. Founders often raise money from friends and family and other angels. The treatment of the friends, family and angels (FFA) as the startup matures and raises larger rounds of financing over time is interesting. Here is a quick guide.

They might have to get another round in, and that round will most certainly be a downround. They might be doing board meetings more frequently, coaching first time founders through layoffs and debating with their partners which companies they should bridge until things thaw out. They're just.

We expect there to be an increase in downrounds, flat rounds, inside rounds and various pay-to-play scenarios. These shut downs are likely to happen when companies are funded solely by seed funds and angel investors that have not reserved significant capital for follow-on investments.

Perspectives on issues affecting founders, startups and investors from a veteran startup lawyer in Silicon Valley. If you are a company that is fundraising, keep in mind that there are a few different levers you can pull to change the amount of dilution that the founders will experience. — 23 Comments.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content