This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many companies are now having to resort to tough measures in order to stay afloat, including layoffs, downrounds and tough terms from current investors. If the answer is yes, then a downround is likely the best path forward. Why you shouldn’t worry about raising a downround ( source ).

New investors hate downrounds. So at GRP Partners we’re very active now. They will enter the “triage phase&# of the market where they figure out which of their existing deals will survive. Many good companies will not get funded. Vultures will start circling looking for deals. Get funded now, if you can.&#.

By contrast, they backed 620 funds in the last three months of 2021 First time fund managers hit hard: In 2022, limited partners backed 141 funds run by first-time managers, a 59% decline from the prior year and the lowest number since 2013 How does the constrained LP environment manifest for funds and startups?

Carta reports that 20% of the rounds in 2023 were downrounds, but I believe the actual number is much higher. For that and other reasons (like cash preservation) VCs moved to focus more on earlier stage, and many funds that typically invest in A started deploying more into seed rounds.

Which VC firm provided the most recent funding round and when was it? If a brand-name VC is an investor, it means that at one time one single partner at the firm saw enough promise in the venture to make a bet on it – it doesn’t mean that a company is doing well now.

Consequently, some startups have faced struggles securing investments, resulting in downrounds where their valuations decline between funding rounds. Additionally, these downrounds can decrease employee morale, as they may dilute shares or pay cuts, affecting the overall work environment.

Of course valuation is in the eye of the beholder but if that VC thinks your last round valuation was way too high then he or she is more likely to politely pass rather than try and talk down your valuation now. VCs hate “downrounds” and many don’t even like “flat rounds.” There are some simple reasons.

As Vintage Venture Partners put it in a recent presentation shared in Tel Aviv , 2022 started off well but fell of a cliff in the second half (the slides were shared on Twitter by Amitai Ziv from Tech 12 ). A report by Greenfield Partners puts the total fundraising of Israeli startups at $15.16 2022 in Israeli tech and venture.

According to Barry Kramer, a partner in the firm and a co-author of the survey, during the third quarter, "up rounds exceeded downrounds 52% to 30% with 18% flat. The report also finds that the best performing industries in the quarter were Internet and digital media companies, followed by those in the life sciences.

No you’re kind of f *d because nobody wants to buy any at all and your bank is calling you concerned that you may need to slow down your pace of new purchases for a bit. Many experienced partners are funds have 7-10 boards and most of these will need more capital. So when prices go down their first reaction is, “S**t.

I was actually somewhat surprised that the following investors have agreed to use the Series Seed documents in certain of the their deals: Baseline, Charles River Ventures, SV Angel (Ron Conway), First Round Capital, Harrison Metal Capital, Mike Maples, Polaris Venture Partners, SoftTech VC and True Ventures.

I always caution entrepreneurs not to take too high a valuation in any round because it sets very high expectations for the next round. A downround, which can damage a company and make it difficult to raise money in the future. He is also a venture partner at several VC firms. What happens then?

Venture capital funds are usually 7 - 10 year partnerships whereby the general partners - the “VC” - manage the capital of the limited partners, usually institutions (endowments, pension funds, etc.). At the end of the period, all profits and proceeds are distributed to the various partners on a pre-determined split.

Mark dutifully went to partner meetings, back-channel references began, firms started calling existing VCs to “test prices” and we started debating whom our best partner would be. Mutual funds had begun marking down the valuations of their private investments in high-profile deals.

They might have to get another round in, and that round will most certainly be a downround. They might be doing board meetings more frequently, coaching first time founders through layoffs and debating with their partners which companies they should bridge until things thaw out.

And if you raise the “5 on 20” and don’t grow into your next-round valuation you’re stuck because venture investors HATE doing downrounds. Some people can skip first base My partner Greg Bettinelli has a sports metaphor that I’ve become fond of which is “skipping first base.”

Some VC firms use the art of Level 3 inputs to mark up their valuations, which has a tendency to make limited partners happy. My easy solution for VC firms would be to mark up or down the valuation of investments based only on new independently led outside rounds of financing. I think this practice is not prudent.

However severe our current situation is, I’m sure there will be plenty of short term negatives, including more job losses, company failures and downrounds. In the ecommerce and marketplace markets Forward Partners operates in growth is limited because business has to scale country by country.

Why I Canceled My CO2stats Account → Quote Of The Day Posted on January 9, 2009 by fnazeeri We intend to continue forward and be very supportive of your downrounds this year.&# This from the head of Intel Capital while speaking at CES (according to Jeff Busang over at Flybridge Capital Partners ).

We expect there to be an increase in downrounds, flat rounds, inside rounds and various pay-to-play scenarios. My partners at JSV have been in the venture business for 14 years and have had the good fortune to be involved in several very large successful companies. 2) Some insiders are supportive.

Interesting strategy, although I don't know if it justifies the added risk of having a flat (or down) round next time you go to raise. Interesting strategy, although I don't know if it justifies the added risk of having a flat (or down) round next time you go to raise. link] Brad Hargreaves. link] Roy Rodenstein.

As someone who invested through the 2001 and 2008 crashes I can assure you that downrounds and fire sales are not fun for anyone involved. There is a silver lining to the recent volatility: a more rational market separates out the noise – for both investors and teams who are looking for experienced, long term partners.

As someone who invested through the 2001 and 2008 crashes I can assure you that downrounds and fire sales are not fun for anyone involved. There is a silver lining to the recent volatility: a more rational market separates out the noise – for both investors and teams who are looking for experienced, long term partners.

As someone who invested through the 2001 and 2008 crashes I can assure you that downrounds and fire sales are not fun for anyone involved. There is a silver lining to the recent volatility: a more rational market separates out the noise – for both investors and teams who are looking for experienced, long term partners.

The situation I see time and again is an over-valuation on a markedly smaller-than-anticipated business, revenue numbers not achieved, and then needing to do another raise on a lower valuation (a ‘down-round’). Who does this investor know in the customer, partner and executive space they can introduce you to? The Rolodex.

Likely signs of a Value investment: the company has challenges in filling out the round; the investors have more negotiating leverage than the founders during the closing process; the company has significantly better metrics (e.g. You could argue that when they were [raising] oversubscribed [VC rounds], Facebook, Google, Amazon, etc.,

I say ecosystem as opposed to industry because it is not just the VC funds themselves that are imploding, instead the collapse includes entrepreneurs and startups that were funded by VCs, angel investors, service providers like lawyers, bankers and accountants as well as limited partner investors in VC funds.

It’s no longer based on a hunch, unless the company is in trouble and needs money to finish what the first round started. This problem often leads to a lowered valuation or “downround” Not a great scenario.) If the company is doing well, the second round is easier to acquire. Accel Partners.

It is not a strong bargaining position for the CEO to ask for money to complete a product promised for completion with the previous round of funding. And professional investors often penalize the company with lower-priced downrounds or expensive loans as a result.

It is not a strong bargaining position for the CEO to ask for money to complete a product promised for completion with the previous round of funding. And professional investors often penalize the company with lower-priced downrounds or expensive loans as a result.

It is not a strong bargaining position for the CEO to ask for money to complete a product promised for completion with the previous round of funding. And we were able to secure that investment along with a partner from that firm joining our board.

The fund managers, who are called"general partners," get about 2% of the fund annually as a managementfee, plus about 20% of the funds gains. Not all the people who work at VC firms are partners. If you get a call from a VCfirm, go to their web site and check whether the person you talkedto is a partner.

All Unicorn participants — founders, company employees, venture investors and their limited partners (LPs) — are seeing their fortunes put at risk from the very nature of the Unicorn phenomenon itself. Their own ego is also a factor – will a downround signal weakness? A downround is nothing.

Greylock Partners · Brian Chesky | People-First Capitalism. So we have to think of ourselves as partners. Our hosts — we have 4 million hosts — most people would have, you might call them, your suppliers, your developers, your partners. And most companies have a partner, group and then society. EPISODE TRANSCRIPT.

Greylock Partners · Brian Chesky | People-First Capitalism. So we have to think of ourselves as partners. Our hosts — we have 4 million hosts — most people would have, you might call them, your suppliers, your developers, your partners. And most companies have a partner, group and then society. EPISODE TRANSCRIPT.

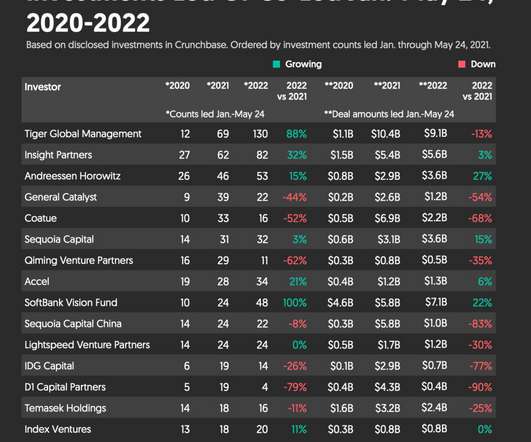

However General Catalyst, Coatue, Qiming Venture Partners and D1 Capital Partners have siginficatedly slowed down their investments based on disclosed data. Interestingly, the investors you’d expect to be holding back (SoftBank. Which Startup Investors Pulled Back The Most So Far In 2022? The bull market is over.

Limited Partners (LPs) who invest in VC funds have continued to pour money into venture – with the market returning to pre-recession levels. Most flat rounds. More downrounds. More structured rounds. State of the Market. The full presentation & data can be downloaded on SlideShare.

It’s an option, even though an expensive one. “ Strategic partner” investors: If you can find a strategic partner willing to invest in your enterprise, consider it a blessing. It is most often a win-win for both you and the strategic partner. Professional angels: This is the arena where I work and play.

Strategic partner” investors: If you can find a strategic partner willing to invest in your enterprise, consider it a blessing. It is most often a win-win for both you and the strategic partner. And even with the significant cost of credit card debt, many entrepreneurs aggressively use existing cards to finance a startup.

It’s this part: “I’m getting inbound from investors…” Nearly all of the inbound VC interest happening out there is from non-partner investors (i.e. A check-writing partner reaches out to you. That’s why downrounds exist. professionals who can’t write a check) and they’re doing it systematically.

It’s an option, even though an expensive one. “ Strategic partner” investors: If you can find a strategic partner willing to invest in your enterprise, consider it a blessing. It is most often a win-win for both you and the strategic partner. Professional angels: This is the arena where I work and play.

Number one is, a lot of companies need to actually educate their customers or their partners, and a lot of that has to happen online. Alexia Tsotsis: Are you seeing downrounds because the NASDAQ is down? Marc Andreessen: No, we have not seen downrounds yet.

But as we’ve seen, these valuations can be hocus-pocus — even at later stage rounds, we’ve seen lots of companies of late fall from grace and become massively devalued overnight when they cannot raise their next round at a higher valuation. If a company raises a good round, it gets marked up to the new value.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content