This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I was reading Danielle Morrill’s blog post today on whether one’s “ Startup Burn Rate is Normal. I love how transparently Danielle lives her startup (& encourages other to join in) because it provides much needed transparency to other startups. ” I highly recommend reading it.

For those of you who have been following the discussion, a Lean Startup is Eric Ries ’s description of the intersection of Customer Development , Agile Development and if available, open platforms and open source. Over its lifetime a Lean Startup may spend less money than a traditional startup. Lets see why.

2 preamble issues having read the comments on TC today: 1: I know that the prices of startup companies is much great in Silicon Valley than in smaller towns / less tech focused areas in the US and the US prices higher than many foreign markets. That’s the deal you get when you’re raising in a good market for startup financing.

The A round was done in February 2000 (end of the bull market) and my B round was done in April 2001 (bear market). As a result I had to do a downround. Downrounds are psychologically really difficult on companies and can make it harder to do later rounds. I eventually needed more money.

I have often been asked about Startup Funding by entrepreneurs. Many myths surround the subject of startup funding. Here is Startup Funding, a Comprehensive Guide for Entrepreneurs. You must have seen a lot of startups giving out promotions, discounts, and incentives at the early phase of their business.

Much has changed in the past four months of the technology startup world and how outsiders value the business. If you raised money in the past 2 years and have grown it is possible that your next round valuation might be flat (or lower) even though you have a higher revenue because investors may value your multiple differently.

A founder asked me what makes a $2M round “pre-seed”? especially if the startup already has a product and revenue? And why do we still sometimes hear about pre-seed rounds that look more like a series A in pricing and size? Defining the pre-seed round It’s futile to look for ‘one true’ definition.

The past year was a wild ride for startups and founders, giving a whole new meaning to the ”rollercoaster” aspect of being an entrepreneur. A combination of competition for top talent and an effort to bring employees back to the office drove startups in Israel to throw extravagant parties and all-inclusive retreats abroad.

Ah, but today’s Internet companies have real revenue! New investors hate downrounds. For others it feels like a two-speed economy, where rules apply to hot tech startups that don’t apply elsewhere. I said that at the Founder Showcase, too. and profits! Many good companies will not get funded.

The market correction has come for series A and seed startups. For the past few week I’ve been sharing here the impact of the current downturn that started in the public markets on startups and venture capital. Until now, early stage startups were relatively unaffected. It’s not just the prices that are coming down.

Want to start a startup? A typical startup goes throughseveral rounds of funding, and at each round you want to take justenough money to reach the speed where you can shift into the nextgear. Few startups get it quite right. A lot of startups that end upgoing public didnt seem likely to at first.

Cram downs are back – and I’m keeping a list. At the turn of the century after the dotcom crash, startup valuations plummeted, burn rates were unsustainable, and startups were quickly running out of cash. A cram down is different than a downround. Cram downs are done by VC bottom feeders.

They won a design award at a trade show, but have no revenue and no orders. As Cuban pointed out, this is a “downround” Zomm is seeking $2M for 10% of the company, implying an $18M pre money valuation today. Kevin questioned the use case since bowls are ubiquitous. The entrepreneur was clearly desperate.

How will you price the next round? Your A round? Revenue multiple? Me: There is no rational explanation for valuations of A round companies by ANY objective financial measure. And now I have to explain to team that they’re taking more dilution than they expected if we do a downround. A downround?

by Rizwan Virk, author of “ Startup Myths and Models: What You Won’t Learn in Business School “. If you are building a startup, you’ll find no shortage of people who are willing to give you advice, particularly when it comes to raising financing. Unfortunately, most startups don’t meet their initial rosy projections.

An ominous title for a blog post, but “Grow or Die” has been one of the most basic rules in the high-growth startup world for decades. And by growth I mean revenue growth. Flat to negative revenue growth is a real red flag, especially for early stage companies. And protection form death. And gasoline to create more growth.

” “Mark has a vested interest in talking down valuations of startups.” Most prefer not to say this publicly for two reasons: 1) they have an entire portfolio of startups, many of whom are raising capital and 2) they prefer not to be attacked publicly or seem “anti entrepreneur.” goes into a startup.

A report by Greenfield Partners puts the total fundraising of Israeli startups at $15.16 Israeli startups 2022 funding summary. Downrounds, especially for growth stage companies, and bridge rounds galore. We started to see downrounds taking place especially in growth stage. billion to $17.1

Industry change allows the entry of newer players at earlier stages – It doesn’t take as much money to launch a startup anymore. So in the past we needed VC to really get a startup going. If you invest it in startups you’re a VC professional money manager. We all know that.

In February of last year, Fortune magazine writers Erin Griffith and Dan Primack declared 2015 “ The Age of the Unicorns ” noting — “Fortune counts more than 80 startups that have been valued at $1 billion or more by venture capitalists.” Next came Rolfe Winkler’s deep dive “ Highly Valued Startup Zenefits Runs Into Turbulence. ”

Below, he gives an honest take about what he’d do differently and what he’d do again as a startup CEO. Rob,” he said, “no offense, but you aren’t going to get a world class, been-there-done-that CEO into a company with less than $1 million in revenue. Startups are incredibly hard. and sold to Datto in late 2014.

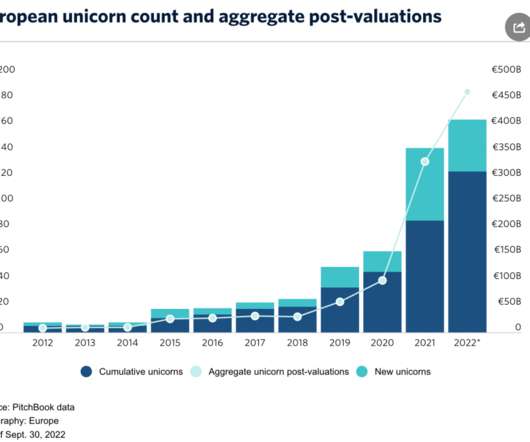

The 2022 Founders Factories report by DealRoom and Accel shines a spotlight on the startup clusters that produced most unicorns across Europe and Israel, and then tracks the alumni of those unicorns to test where the talent goes to found their next companies. London and Tel Aviv are home to the most founder nurturing unicorn startups.

No one can predict the future and it’s especially true in the startup world. The statistics show that even though most founders bet their time and resources that their startups will be the best in the world, 90% of those new startups won’t be in operation in 10-15 years. Sensitivity Analysis: “What if my assumptions are wrong?”.

I have written about startup valuations previously. If you are advising startup founders, I strongly suggest having them read all 4 of the posts to get the lay of the startup valuation land. A founder is about to raise their first round and asking me how to value their company. [1]. Here is a post from October 2012.

Investors had grown too used to the idea that any deal you funded would get marked up to a higher valuation in the next round and that’s clearly not always true. Invoca was raising at the tail end of this market phenomenon at this time doing tens of millions in SaaS recurring revenue and growing at a nice clip. FOMO was NOMO.

We must #BRINGTHEMALLHOME August was a slow month in venture investment as globally startups raised $18 billion in August worldwide, a 37% decline MoM and 24% decline year over year. This was also felt in Israeli startups, who reportedly raised only $201M in 7 deals, bringing the total to $938 million in 61 deals in Q3 2024 so far.

This venture capital financing - usually between $3 and $10 million - is the first of a number of rounds of outside investment over a period of three to five years. With this capital, the company propels itself to $50 million+ in revenues, and to either a sale to a strategic acquirer or to an initial public offering.

To meet growth and revenue targets, you hire and spend like never before. You fall into the spiral of death: head of sales gets replaced (at least once), CEO gets replaced (at least once), a down-round financing happens (if lucky). Startup general interest Venture Capital'

If you run a startup and are currently raising money, you probably planned for a somewhat different fundraising environment than the one you find yourself in today. Perhaps you are caught in the “Series A crunch” or perhaps you are a consumer company and expected that you would be valued on users rather than revenue like the last time.

As I’m sure most would agree, Airbnb is one of the most iconic startups to have been formed in the world. But I generally am not a fan of committees and things that get in the way of moving quickly in a startup. But now our hosts are really angry, and they have a huge revenue shortfall. Not that we should have more committees.

Startups and angels: Along the way to success. " The problem has been that too-high valuations and too generous terms have spawned painful downrounds that squash the entrepreneur and his early investors. up to $10MM in revenue. up to $10MM in revenue. up to $10MM in revenue.

Some businesses require very little capital and the founder can self-finance the enterprise and retain 100% of its ownership and control from ignition through liquidity event (startup through sale). And even with the significant cost of credit card debt, many entrepreneurs aggressively use existing cards to finance a startup.

In order to launch a successful business and raise the capital needed to do so, a startup needs to consider several aspects of the business including the management team , the size of the opportunity, the product/service/technology, the market/sales/distribution channels, the competitive environment and several other factors.

Some businesses require very little capital and the founder can self-finance the enterprise and retain 100% of its ownership and control from ignition through liquidity event (startup through sale). And even with the significant cost of credit card debt, many entrepreneurs aggressively use existing cards to finance a startup.

You may recognize these five as a slight variation on the “Berkus Method” which is often published and used by investors when valuing pre-revenue businesses. Here we expand the definitions a bit to encompass businesses that are still early stage, but perhaps beyond startup. And fifth: Competitive risk. .

Some will demonstrate strategically justifiable metrics and have fantastic ‘up round’ exits; others may see liquidation preferences kick in which will negatively impact founders and employees; others may fulfill the adage “IPO is the new downround” , which has been the case for more than half of the public companies on our list.

As I’m sure most would agree, Airbnb is one of the most iconic startups to have been formed in the world. But I generally am not a fan of committees and things that get in the way of moving quickly in a startup. But now our hosts are really angry, and they have a huge revenue shortfall. Not that we should have more committees.

Some businesses require very little capital and the founder is able to self-finance the enterprise and retain 100% of its ownership and control from ignition through liquidity event (startup through sale). And even with the significant cost of credit card debt, many entrepreneurs aggressively use existing cards to finance a startup.

It takes a long time to see the results of a startup that does well. But as we’ve seen, these valuations can be hocus-pocus — even at later stage rounds, we’ve seen lots of companies of late fall from grace and become massively devalued overnight when they cannot raise their next round at a higher valuation.

I waited for the ‘casino-like’ world of startup investing until I was 28 years old, putting $10,000 into a friend’s software distribution company – a tidy sum for me at that age. Soon after that first investment, I started my first business, and am now on my fifth (all $1m+ in revenue, but not all ‘successful’).

If you run a startup and are currently raising money, you probably planned for a somewhat different fundraising environment than the one you find yourself in today. Perhaps you are caught in the “Series A crunch” or perhaps you are a consumer company and expected that you would be valued on users rather than revenue like the last time.

I say ecosystem as opposed to industry because it is not just the VC funds themselves that are imploding, instead the collapse includes entrepreneurs and startups that were funded by VCs, angel investors, service providers like lawyers, bankers and accountants as well as limited partner investors in VC funds.

The Second Round, or “B Round”, or “Follow On” round can be the achilles heel of a startup. No doubt the first round of external funding for a startup is usually critical to a startup as it can be the difference between continuing your startup or shutting it down.

Building on my post on ‘ Advice for startups in a downturn (May 2022 edition) ‘, this week I continued to follow with interest the impact of the current correction on startups and venture capital, particularly in early stage. Which Startup Investors Pulled Back The Most So Far In 2022? The bull market is over.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content