This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Something happened in the past 7 years in the startup and venture capital world that I hadn’t experienced since the late 90’s — we all began praying to the God of Valuation. It wasn’t always like this and frankly it took a lot of joy out of the industry for me personally. What happened? How might our next phase of the journey seem brighter, even with more uncertain days for startups and capital markets?

As a long-time business advisor and angel investor, I’m a believer that “two heads are better than one” in building a new business. Very few entrepreneurs have the range of skills and experience to be the solution creator as well as business creator, or operational as well as sales leader. The challenge is to recognize and recruit that ideal partner match early with minimal cost and risk.

This post previously appeared in Fast Company. How does a newly hired Chief Technology Officer (CTO) find and grow the islands of innovation inside a large company? How not to waste your first six months as a new CTO thinking you’re making progress when the status quo is working to keep you at bay? I just had coffee with Anthony, a friend who was just hired as the Chief Technology Officer (CTO) of a large company (30,000+ people.

Welcome back. Hope you had a relaxing break and are ready for a hectic, very different 2022. Actually, “very different year” has been our annual guiding principle and reflects Deal Architect’s business model. Every year our revenue stream varies and.

Speaker: Nick Noreña, Innovation Coach and Advisor, Kromatic

Every startup and innovation project exists within an ecosystem that either helps or hurts that project. As innovation managers, we need to keep a pulse of that ecosystem and make sure we're helping those innovation projects we're managing every step of the way. In this webinar, Nick Noreña will walk through an Innovation Ecosystem Model that he and his team at Kromatic have developed to help investors, heads of product, teachers, and executives understand how they can best support innovation in

According to Bert Thornton and Dr. Sherry Hartnett, a mentoring program might just become your secret weapon in navigating uncertain, chaotic times and coming out on top. Here are nine ways mentoring can help you meet the challenges of 2022. The post Nine Reasons Why Your Company Should Create A Mentoring Program in 2022 appeared first on Young Upstarts.

It’s become a cliche in our technology startup world: disruptive technologies start as toys and are dismissed as such. The criticism gets louder as the realization starts setting in… the realization of just how much the tech will truly change the status quo. In the creative realms of music, written word, and visual imagery – previous new technologies have encountered this skepticism. .

At our mid-year offsite our partnership at Upfront Ventures was discussing what the future of venture capital and the startup ecosystem looked like. The market was down considerably with public valuations down 53–79% across the four sectors we were reviewing (it is since down even further). ==> Aside, we also have a NEW LA-based partner I’m thrilled to announce: Nick Kim.

At our mid-year offsite our partnership at Upfront Ventures was discussing what the future of venture capital and the startup ecosystem looked like. The market was down considerably with public valuations down 53–79% across the four sectors we were reviewing (it is since down even further). ==> Aside, we also have a NEW LA-based partner I’m thrilled to announce: Nick Kim.

These days, it is almost impossible to find a small business where everything is done by full-time employees, in the office or at home. We are in the age of outsourcing, by any of many popular names, including subcontracting, freelancing, and virtual assistants. These approaches allow your startup to grow more rapidly, save costs, but costly mistakes can lead to business failure.

The “valley of death” is a common term in the startup world, referring to the difficulty of covering the negative cash flow in the early stages of a startup, before their new product or service is bringing in revenue from real customers. I often get asked about the real alternatives to bridge this valley, and there are some good ones I will outline here.

One of the biggest myths in the business world is that startups are no place for Baby Boomers, that aging generation born between 1945 and 1964. They couldn’t possibly understand the new social media culture, new technologies, or have the determination to beat their younger counterparts in the market. Yet credible reports on current trends tell us just the opposite.

With the ITRC 2021 End-of-Year Data Breach Report revealing a 68 percent increase in stolen sensitive personal information, there is a growing population out there worried about all the people intent on hurting them. My recommendation to entrepreneurs is to recognize these concerns as an opportunity to make people’s life better, rather than worry and dodge the risk.

Startup investors tell me they invest in a new venture with a higher caliber of people, rather than the product or service, and I agree. In my role as a business advisor, I see successful businesses most often emerging from great teams rather than great products. Yet I find the people building teams are usually product experts, often with no experience in team building.

Valuing a business based on assets and financial performance is a well-understood process, but every investor knows the real value goes well beyond these parameters, either higher or lower. The key elements of leadership in a company, both individual and organizational, are less tangible, but very critical in setting a market value for investment, acquisition, or going public.

Even in this age of globalization and virtualization, the geographic area where you choose to live and work can still make or break your startup business. I still have to tell some entrepreneurs that even with the best idea, they have to move to Silicon Valley to find the investors they need, or they need to move to the U.S. get the attention of the market they choose.

If you are like most entrepreneurs I know, there just aren’t enough hours in a day to get all your own work done, as well as run the many one-hour meetings each team member seems to demand for decisions and mentoring. I have found it to be more productive and effective to lead with the model that no meetings will take an hour, and may be done in as little as five minutes.

Most small businesses have now forgotten the recent pandemic, and are back to “business as usual.” They don’t realize that business as usual is gone forever. With social media and smart phone apps, real product information spreads at astounding speeds. Entrepreneurs that are not listening, not engaging, and not changing are destined to be left behind even in the best of times.

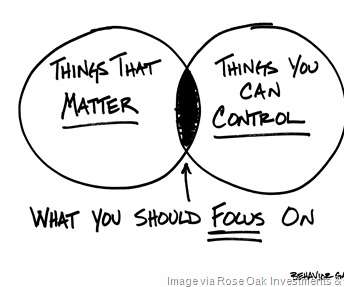

Everyone in the business world has heard of the classic bestseller by Geoffrey A. Moore titled “ Crossing the Chasm ,” but most entrepreneurs have no idea how it relates to them. In fact, it’s all about the “focus” required to get early stage technology products across the deadly chasm from early adopters to mainstream customers. Most investors and startup professionals expand this concept of focus to apply to key issues of every aspect of strategic and tactical planning in a startup.

New entrepreneurs tend to focus only on getting the product right, and assume that the right culture and ethics will come later simply by hiring good people. In fact, they need an early focus on developing their moral compass, as well as setting the right ethical tone. Building an ethical business is more than just compliance and meeting legal requirements, and it has big paybacks.

When it’s time to sell your company, or get new investors, valuation is the key parameter to success or disappointment. The first step is to quantify the value of assets and current financial performance, but every one of you wants to go further by adding additional value for “intangibles,” commonly called goodwill. The challenge is what and how to highlight these to your advantage.

Today more than ever, the evidence is clear that business people need to find and communicate a purpose that goes beyond making a profit, in order to ensure customer engagement, as well as your own, and drive results in the marketplace. In my work with entrepreneurs, I have concluded that finding and communicating that purpose is often more important than the solution offered.

I see more and more entrepreneurs who seem to have everything going for them – vision, motivation, passion, even a good business plan, product, and money, and yet they can’t close customers. Maybe it’s time to look harder at the mantra of a new breed of gurus and successful entrepreneurs, including Steve Blank and Eric Ries , called “nail it then scale it” (NISI).

I have learned from experience that scaling any business is difficult. You may feel good when that first burst of customers arrives, but don’t assume that “ word of mouth ” and those early adopters will grow your business to match your dreams of success. In these days of global competition via multiple channels, you need continuous marketing to find more customers.

Even if you ignore all the hype around crowdfunding, there can be no doubt that it is a real alternative for entrepreneurs to achieve visibility and funding today. According to a classic article on Thrinacia , there were over 600 crowdfunding platforms in existence then, estimated to add more than $89 billion to the economy at a compound growth rate of 17% from 2019 to today.

Successful startups seem to follow similar paths to greatness, and unfortunately all too often that path leads them back down the hill much faster than they went up. Big company powerhouses, like IBM and Xerox, took fifty years to make the cycle, but new companies today, in the age of the Internet, often make the cycle in five to ten years, or even less.

Based on many years of experience in business as an executive and consultant, I have long been convinced that emotional intelligence (EQ or EI) in leadership wins over logical intelligence (IQ) every time. The experts define emotional intelligence as a leader's ability to recognize individual and team emotions, to understand their effect, and manage your own to guide your next move.

Marketing is everything these days. You can have the best technology, but if customers don’t know you exist, or they don’t know how your technology solves a real problem for them, your startup will fail. Yet I see many technology entrepreneurs that focus on the basics of marketing too little and too late. They skimp on the design of their website, procrastinate on the rollout to make sure the product is perfect, and get so excited about technology features that they forget about creating value f

Every entrepreneur and business leader I know realizes that it takes a dedicated team to build and run a successful business, and nurturing that team is one of your most important priorities. Yet I find, as a mentor and outside consultant, that many of you focus only on working conditions and compensation as the key factors determining team engagement , health, and productivity.

Most business mentors tell me that the single biggest problem they have to deal with in small companies is the lack of open, honest, and effective communication, both from the top down and from the bottom up. Some entrepreneurs forget that talking is not communicating. Fortunately these skills can be learned, and the barriers to communication can be overcome one by one.

Perhaps sparked by the recent pandemic, I’m seeing a new era of the entrepreneur, with startups springing up all around. Based on my own mentoring and investing experience, the best entrepreneurs are pragmatic problem solvers. They have an uncanny ability to find elegant, easy, and fast solutions to pain points in the marketplace, as well as their own challenges.

Every startup lucky enough to get some traction gets to the point where they decide to hire some “regular employees” for sales, marketing, and administrative tasks. Then they are surprised to see productivity and creativity take a big dip. What they should be doing is hiring only “entrepreneurs,” meaning people who think and act as if this is their own business.

Angel investors and venture capitalists don’t make equity investments in nonprofit good causes. The simple reason is that it’s impossible to make money for investors when the goal of the company is to not make money. Yet as an active angel investor, I still get this question on a regular basis, so I’ll try to outline the considerations in common-sense terms.

One of the things I’ve learned over my years as a business mentor and investor is that life isn’t fair when it comes to succeeding in business. You may think that passion and hard work are all you need, but I believe we all have unique strengths , and you need to recognize yours, and capitalize on them above all else, in order to get the advantage you need to win in business.

People who have been followers too long as an employee don’t realize how hard it is to be a leader. Every new entrepreneur has to initiate the right actions to be perceived as a leader in their chosen business domain by their team and by their customers, or the road to success and satisfaction will be lost along the way. Driving these actions are some basic principles that entrepreneurial leaders, such as Airbnb CEO Brain Chesky and LinkedIn CEO Jeff Weiner, seem to have learned early.

Every entrepreneur and business leader waits too long before really working on the legacy that he wants to leave to society and his family. They realize too late that they don’t really want to be remembered for how many hours they spent on airplanes, how many emails they produced, or even how much money they made for the business. If you disappeared today, what would your legacy show?

Large corporations and conglomerates, the engines of growth and vitality in the twentieth century, have lost their edge and their image. They have proven themselves unable to innovate, and they have lost more jobs than they create. My friends who “grew up” with lifetime careers in General Motors, Exxon Mobil, or even IBM, are now often too embarrassed to even mention it.

Business partners can be co-founders in a startup, multiple owners of an existing business, or a joint venture. In every case, a partner can be an asset, bringing new skills and perspectives to the business; or a burden, making every decision more difficult, and taxing your lifestyle satisfaction. You need to do the due diligence to make that decision before you sign away your equity.

In my years of advising startups and occasional investing, I’ve seen many great ideas start and fail, but the right team always seems to make good things happen, even without the ultimate idea. That’s why investors say they invest in people (bet on the jockey, not the horse), rather than the idea. Yet every entrepreneur I meet wants to talk about the idea, and rarely mentions the team.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content