This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When I first read Paul Graham’s blog post on “High Resolution&# Financing I read it as a treatise arguing that convertible notes are better than equity. Either would be fine with startups, so long as they can easily change their valuation. Photo credit: D. Blanchard/O’Reilly Media. When I’m in, I’m in.

We drew this conclusion after a meeting we had with Morgan Stanley where they showed us historical 15 & 20 year valuation trends and we all discussed what we thought this meant. But rest assured valuations get reset. When you look at how much median valuations were driven up in the past 5 years alone it’s bananas.

Why do these founders get to stay around? Because the balance of power has dramatically shifted from investors to founders. VCs competing for unicorn investments have given founders control of the board. A pre-IPO board usually had two founders, two VCs and one “independent” member. Technology Cycles Measured in Years.

Founders vs. Early Employees To help with this discussion, let me start with a definition of "early employee." The first few people into a startup are on a spectrum of founder vs. early employee. Founders are likely not paid for a long time and have a sizeable equity percentage for early risk and having the concept.

Business valuation is defined as a way to determine the overall economic value of a company , and is a necessary component of a sound business plan and strategy. Any of these situations will demand a valuation to determine current and future projected value. . Three Methods of Valuation. Life happens to all of us.

I recently spoke at the Founder Showcase at the request of Adeo Ressi. I said that at the Founder Showcase, too. In addition to FOMO it is partly driven by massive increase in valuations for earlier-stage companies who raised money at bit seed prices but who still have product risk. This post originally ran on TechCrunch.

2: As expected at least one person accused me of writing this post because I want to see lower valuations. I’ve decided to take all of my private conversations and subjective points-of-view on the topic and make them public in a keynote speech at the Founder Showcase in San Francisco on June 15th. That’s stupid.

Before the rapid rise of Unicorns, (startups with a valuation over a billion dollars), when boards were still in control, they “encouraged” the hiring of “adult supervision” of the founders after they found product/market fit. The founders. Founders are comfortable in the chaos and disorder. Adult Supervision.

Was Paul Graham right in his “high resolution” financing post? What the entrepreneurs were really saying is, “I don’t want to take a lower valuation now, while I don’t have customers or a full team. Convertible debt WITH a cap is stupid for founders. Some thoughts on raising angel money.

We received so much positive feedback from our This Week in Venture Capital show walking through valuation calculations & term sheets that we decided to do a Q&A show this week to address topics that entrepreneurs want to learn about. The best thing to get is a “right sized&# valuation. A: It’s not best.

November 23, 2010 Entrepreneurs, Using Outsourcing to Obtain Capital Efficiency Needs to be Thought Through to be Effective - Robert Ochtel , June 7, 2010 Teen Entrepreneur, Brian Wong, Youngest Founder to Receive Angel Funding - teenentrepreneurblog.com , October 28, 2010 Build Your Own Silicon Valley?

A founder asked me what makes a $2M round “pre-seed”? While the answers are somewhat semantic, the pre-seed funding round is making a comeback in 2024 startup financing. especially if the startup already has a product and revenue?

My friend Michael Broukhim, founder & co-CEO of FabFitFun and I recently had a catch-up meeting for 3-miles on the Santa Monica “Bird Trail” No company has ever elicited so many questions by friends, colleagues, entrepreneurs, fellow VCs and journalists as has Bird, the company that pioneered the electronic scooter as a service market.

Mike is a no BS guy, has all the attributes I look for in a founder and says things like, openly shares knowledge and opines without a filter including this one, “whoever invented uncapped convertible debt should be spanked!&# This is an interview you’re not going to want to miss, I promise. Contest details here :

Should I trust my instincts for founders and products or should I be more focused on the market size or business plan? ” As far as “terms” go I’m 100% aligned to have the most vanilla, founder-friendly terms I can. And I listen to the reasons their co-founders quit their well-payed job to join them.

Should I trust my instincts for founders and products or should I be more focused on the market size or business plan? ” As far as “terms” go I’m 100% aligned to have the most vanilla, founder-friendly terms I can. And I listen to the reasons their co-founders quit their well-payed job to join them.

They should heed the age old advice that raising slightly more money while you can is always better than trying to optimize future valuations. Should VC’s really be impacted by public market valuations when the money that they’re investing today should be for returns in 7-10 years? Short answer – yes.

why the hell has seed financing declined so much in the past 3 years?? And this era ushered in by Amazon changed everything from the age of founders to the skill sets required to the structure of the VC industry and even to the layout of cities (yes, I would proclaim that boldly that Amazon AWS affected city development).

” If you invested at $8m pre-money and put $2m in (thus you own 20% of a company at a $10m post-money valuation) and if you put another $2m into a round at a $40m valuation raising $10m ($50m post) you end up with half your money at $8m pre and half at $40m pre thus your average price goes up dramatically. Thus begins the dance.

With all other things equal, that means that a 50/50 split between two co-founders (evenly split if there are more than two), or a 66/33 split based on the premium for coming up with the original idea, and for starting the initial development efforts and sourcing the original team. To me, that is no different than financing the business.

As the idea went from innovating on software & systems to launching a company to rolling it out in the field brought on Rahul Gandhi as his co-founder to physically launch the company. Sam & Rahul have worked closely together on “innovate & operate” since the earliest days of MakeSpace. Seriously, this happens.

Using NextView as an example, since we both seek to lead the seed round and only lead during this round, I’ve seen this trend manifest in one of two ways: In a priced round, the entrepreneur will often share their valuation ask (or a stated floor) for the pre-money valuation of their company much sooner in the process.

When you look at a deal so much of what you’re trying to understand are the skills, resiliency , work ethic, motivation and team dynamics of the founders. Nothing blows up great opportunities faster than founders who are constantly fighting. There are times you just need help getting s**t done.

There may be some twists and turns along the way, like a bridge or seed extension, but I think something like this is plan A for most founders. Unless a founder has angels interested who are not really price sensitive, a founder might find themselves selling a pretty big chunk of their company for not that much money.

The following is a condensed explanation of seed funding: Seed money is a form of early-stage financing that new businesses receive from investors in exchange for a share of ownership in the company. The term “seed financing” refers to the stage of funding that comes from first equity. What exactly is the seed funding?

The founders were simply wrong about their assumptions about customer needs. It turns out the term “visionary founder” was usually a synonym for someone who was hallucinating. Founders Need to Run the Company Longer. So, almost like clockwork 20 th century startups fired the innovators/founders when they scaled.

I read commentary or Twitter or blogs and realize that there are also strongly held convictions that there are these evil VCs who do terrible things to mostly altruistic founders. But unlike the popular press reporting of this conflict — 80% of the time it is founder-to-founder conflict and not investor-to-founder conflict.

If polled a week before the board meeting a good number of founders would say, “I wish we could delay this meeting a couple of weeks” or “I really could do without having this board meeting at all.” The law firm has done its job of preparing the stock option requests, board meeting minutes, 409a valuations. There are too many pages.

They were referring to non-founder engineers, most commonly the first hire for technology businesses. is frequently granted ownership significantly less than that of the founders. However, at the very early stage, they are taking as much risk with their future as the founders. Engineer #1?

Here’s the punchline: if you run your company as if you have closed a VC equity financing round even though you actually closed a convertible debt round, you’ll be in much better shape when it comes time to raise your Series A financing. The investors, founders, and “community” are all super excited about ASC.

I have interacted with a lot of founders who funded their initial business expenses through credit cards. If you are facing any problem you can always check out this: Business Loan vs. Equity Financing. The bridge or exit stage is generally of very large transactions and for companies with substantial valuation. Inception stage.

The startup industry may be “resetting,” which doesn’t mean a “crash” but rather just a resetting of valuations, timescales, winners/losers, capital sources and the relative emphasis of growth rates vs. burn rates. Founders hate them because they’re dilutive. Be realistic on valuation.

Also, if there is a lowering of M&A activity this will lead to increased financing needs for startups driving higher failure rates or increases in “adverse terms” entering future financing rounds. Either won’t bode well for angels if they’re also hurting on non tech investments. What does this mean if you’re an investor?

At the turn of the century after the dotcom crash, startup valuations plummeted, burn rates were unsustainable, and startups were quickly running out of cash. They offered desperate founders more cash but insisted on new terms, rewriting all the old stock agreements that previous investors and employees had. They’re Back.

This article highlights their advice on issues ranging from financing to patent trolls: While startups may believe lawyers are too costly, working with one early on avoids potentially serious problems later. “And if you have a valuation cap; a higher cap is always better than a lower cap.” ” The Cost of Financing.

Arif Bhalwani is the co-founder and CEO of Third Eye Capital (TEC) in Toronto, Canada. TEC is one of Canada’s largest and most experienced private credit firms, specializing in providing asset-based capital solutions to companies that are underserved or overlooked by traditional sources of financing, primarily banks.

Once you have a potential investor excited about your team, your product, and your company, the investor will inevitably ask “What is your company’s valuation?” The founders now need a $1M Angel investment to do the marketing for a national NewCo rollout, build a team to manage the rollout, and maybe even pay themselves a salary.

How else can you explain this headline matching a story about a professional social network still trying to explore revenues raising $17mm on an $80mm valuation? Did I mention it only took the founder a month? I suppose, more specifically, the bubble ended in the last two weeks of September--right after this financing.

Foundry Group is best known for our investments in startups, but our vehicle currently investing in other venture funds, Foundry Group Next, is off to what we believe to be a great start and I wanted to share an update about it by talking about our new investment in a fund managed by Founder Collective.

Over the last 10 years, we’ve been in a bull market with considerable froth in late stage financing activity and valuations. The cases of WeWork and Uber cast a cloud of doubt over funds that are largely driven by one or two outlier companies that may have a tremendous valuation, but shaky underlying business metrics.

The founders were very sympathetic; a man, laid off from his job, and his very pregnant wife, who sold their house and investing $150k into the business and are working hard to make a go of it. The two founders invested $40k in the business, and plan to license it rather than manufacture it because manufacturing seems too hard.

What Are Your Valuation Expectations? But mainly we did it because these corporate VCs were among the only groups willing to invest at PayPal’s somewhat inflated post-money valuation, during the middle of the dot-com crash when traditional VCs pulled back sharply and other sources of funding were constrained.” ” (Rob Go).

Once you have a potential investor excited about your team, your product, and your company, the investor will inevitably ask “What is your company’s valuation?” How much is NewCo worth to investors at this point (pre-money valuation)? This is the most concrete valuation element, usually called the asset approach.

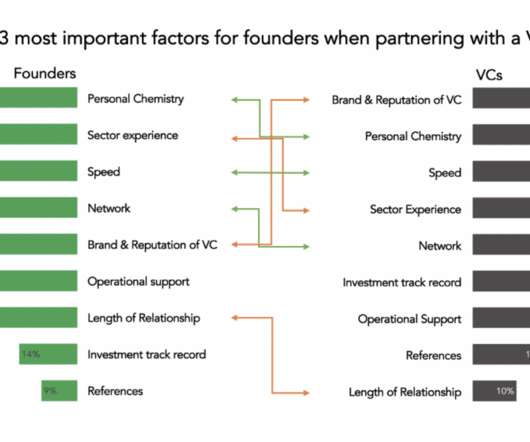

Most founders don’t feel they are getting value from their investors, even in areas like follow on rounds where they would hope to see specialized experience. But how impactful is all of this according to the people who actually matter – venture-backed CEOs? The answer may surprise you. Creandum’s recent article, Do VCs add value?

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content