This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

— Unremarked and unheralded, the balance of power between startup CEOs and their investors has radically changed: IPOs/M&A without a profit (or at times revenue) have become the norm. In the 20th century tech companies and their investors made money through an Initial Public Offering (IPO).

Posted on September 14, 2009 by steveblank Over the last 30 years Wall Street’s appetite for technology stocks have changed radically – swinging between unbridled enthusiasm to believing they’re all toxic. Your firm worked with an investment banking firm that underwrote and offered stock (typically on the NASDAQ exchange) to the public.

The belief then was that most founders couldn’t acquire the HR, finance, sales, and board governance skills rapidly enough to steer the company to a liquidity event, so they hired professional managers. It was so compelling, everyone worked extremely long hours, for little pay and some stock.

On a public stock market that is the value that investors place on future free cash flows of the business discounted to today’s date to account for the time value of money. The price of public stocks change instantly in reaction to news that is perceived to affect the future value of that company. Here’s what I mean.

And this is happening in mezzanine (pre-IPO) deals as well. And post IPO deals, although these tend to correct more quickly. If everybody is over-paying for early-to-mid stage deals you’d imagine that these all need to feed into a frenzied M&A and IPO market that will garner big returns for these risks investors are taking.

But VC is an “illiquid asset&# so funds didn’t disappear quickly - In 2000/01 the stock market quickly adjusted punishing investors in the NASDAQ and in individual public technology stocks. What accelerated this was the collapse of the public stock markets. But in bad economies many angels get burned.

There are obvious reasons the industry has had less-than-desirable returns, including: massive over-funding of the sector, huge increases in inexperienced venture capitalists that took a decade to peter out, and the massive correction in the value of the public stock markets that closed many exit opportunities for half a decade.

Stock exchanges is a growing industry where stock investors interact with various companies wishing to exchange the shares. For startups and entrepreneurs, awareness of the stock exchanges will help prepare you for a potential public financing of your company through an initial public offering, known as an IPO.

On July 27th, 2001 Accenture IPO’s and many of the partners grew fabulously wealthy. Since that date the S&P 500 is up 2.45% while Accenture stock is up 206% with revenue of $23 billion and a market cap of $32 billion. Arthur Andersen was embroiled in the Enron scandal and forced out of business.

My original thinking from Oct ’09 was, while I didn’t (and still don’t) have a crystal ball I worried that: consumers were over-stretched with debt (and make up 77% of the economy), unemployment would continue to rise, which in turn would drive the stock market south and cut the rate of M&A activity and VC investment even further.

In addition, they can neither issue stocks nor bonds. Lower tax rates allow an LLC to be more flexible with finances. However, most institutional investors (venture capital groups, for instance) don’t mind this structure, and they, in fact, prefer to invest in corporations due to protections from issuing stocks.

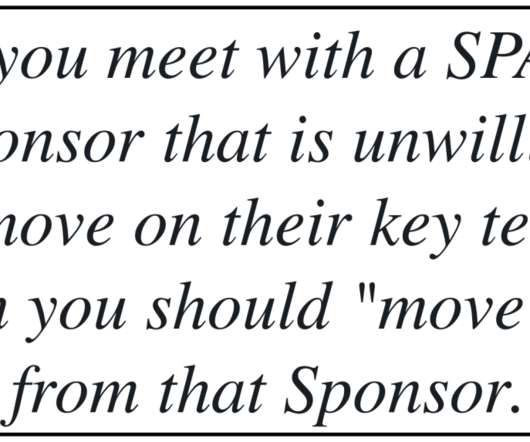

But in light of where we are in 2020, especially with regard to the degrading efficiency and sky-rocketing cost of capital through the structurally broken IPO process, SPACs may emerge as a legitimate third option for helping Silicon Valley companies efficiently and cost-effectively transition into the public markets.

In the old days there weren’t many fights about whether angels would take their prorata rights in financing rounds. Have you noticed the increase of founders selling their personal stock in what is known as a “secondary?” Thus begins the dance. Why prorata rights used to be less of a big deal to angels.

Modern theories of economics and finance teach us that in a world of perfect information, the market will decide what a fair price is for any company’s stock at any point in time based on its current financial condition, results of past operations, analysts’ forecasts of future performance, industry conditions and so on.

As stated earlier, investors will dilute ownership upon nearly every round of financing. Is there an IPO story here? Again this is somewhat simplified as the liquidity event (sale or IPO) may come as cash, stock, or a combination of the two. Stock is naturally more speculative as to value, public or private.

Initial Public Offering (IPO). Initial Public Offering (IPO): This exit strategy is not suited to most small businesses, primarily because it means convincing both investors and Wall Street analysts that stock in your business will be worth something to the general public. Types of exit strategies. Management buyout.

Three reasons: There is a relative valuation between the price a VC pays and their expectations of what it will exit for in an IPO or trade sale. The professor plotted data and showed us statistically that most people buy stocks when they are booming (e.g. Short answer – yes. The best MBA class I took was an investment strategy class.

Startups have some unique struggles, especially in regard to financing. You’ll be entirely responsible for the future of your company and it will be down to you whether or not you run it for the rest of your life or decide to sell, merge or launch it on the stock market. Key difference #2 – the relationship with funding.

Options are gravy - I lived through the first dot com era where we used stock options as a recruiting tool. We set our sites on our IPO price and then worked back to our current valuation and showed potential employees what we thought they could earn (with all legal caveats) if the company was successful. We give out stock options.

Even though the Initial Public Offering (IPO) alternative for a successful startup seems to be coming back into vogue, it is relatively rare. IPOs in 2008, the market was up to a still trivial 159 in 2011. Consider the recent example of Facebook and Mark Zuckerberg. After a record low of 39 U.S.

Inox India’s initial public offering ( IPO ) opened on Dec. 18, with the IPO scheduled to be allotted on Dec. It will make its stock market listing debut on Dec. crore (Rs 14593200000, or $175,110,373.74) with the IPO, with the company itself receiving nothing for the sales. Photo credit: DALL-E.

Even though the Initial Public Offering (IPO) alternative for a successful startup seems to be coming back, it is relatively rare. IPOs in 2008, the market was up to a still trivial 128 in 2012 (compared to 675 in 1996). business entrepreneur exit founder IPO startup' Consider the recent example of Facebook and Mark Zuckerberg.

If you never have, you can create your own using Google Finance. Sure I can build a stock chart, like this one , that shows that eBays stock price went into a four-year decline immediately after "eBay Inc Acquires Dutch Company Marktplaats.nl." If you never have, you can create your own using Google Finance.

Finance is about reporting on historical performance and future planning through the lens of financial metrics.” Two Hires Startups Wait Too Long To Make “The first hire is a really good business generalist that is focused on analytics, finance, and ops. Why Do Consumer IPOs and B2B IPOs Get Treated Differently?

Ultimately what will give you the best chance for success is focusing on the things that you can control – building a real business with a real economic model that can generate cash from internal operations vs. through external financing. As he discusses in his blog post: Why I decided to pull our IPO filing. Market conditions 2.

2019 is off to an exciting start for IPOs of VC-backed startups. In some respects though Zoom has had the most “successful” IPO of the three companies, which has surprised some folks. In the last decade or so, high profile consumer IPOs have often gotten lofty valuations.

Twitter’s IPO has garnered a ton of attention in the tech and popular press. So their revenue figures, pre IPOfinancing and ownership, and other info is all widely available. Growth IPOs Are Back. Instagram hadn’t built a true business (e.g. Value of Media vs E-Commerce vs Premium Services.

” As a result, Ted introduced the Series Seed preferred stock documents as an alternative to convertible debt for early stage investments. One major concern about convertible debt is that it eventually needs to be repaid if another round of financing doesn’t occur. The problem. Series A) or have to be repaid.

In addition, they can neither issue stocks nor bonds. Lower tax rates allow an LLC to be more flexible with finances. However, most institutional investors (venture capital groups, for instance) don’t mind this structure, and they, in fact, prefer to invest in corporations due to protections from issuing stocks.

Every successful technology company raises money throughout its lifecycle, perhaps starting with a seed investment and progressing through Series A, B, C, late-stage investments, and, for the most successful companies, an IPO. An unprecedented 80 private companies have raised financings at valuations over $1B in the last few years.

Gregory Wehmeyer True, Ben, once upon a time, Angel Investors provided the launching pad for Venture Capital Firms to propel any startup on two legs toward a successful IPO. We are coaching VCs and Angel Investors everyday who call us wanting to understand our Early Stage LPO versus late stage IPO approach to business.

Gregory Wehmeyer True, Ben, once upon a time, Angel Investors provided the launching pad for Venture Capital Firms to propel any startup on two legs toward a successful IPO. We are coaching VCs and Angel Investors everyday who call us wanting to understand our Early Stage LPO versus late stage IPO approach to business.

It’s meant to support and grow a business until an “exit” in the form of an IPO, a merger or acquisition, or in less than ideal scenarios, a company shutdown. And, if you’re a public company, you get daily real-time feedback on at least the perception of your progress, as measured by the stock price. What about in the public markets?

Entrepreneur Homepage Startups Starting a Business Home How-To Guides Startup Basics Business Ideas Business Planning Startup Financing Success Stories Home-Based Business Starting a Business Play Video How to Take a New Product from Just an Idea to a Business (Video). Financing Some Jobs Act Proposals Make Headway.

Ultimately what will give you the best chance for success is focusing on the things that you can control – building a real business with a real economic model that can generate cash from internal operations vs. through external financing. As he discusses in his blog post: Why I decided to pull our IPO filing. Market conditions 2.

The value ascribed by subsequent investors (in a secondary); buyers (acquisition); or the public markets (IPO). Eligible for favorable treatment under Qualified Small Business Stock exemption, if structured as equity. This applies if the investment converts into common stock; details are beyond this essay’s scope.

We did the early round of financing and the founding team walked when the market turned and when the situation got tough. It will likely IPO in the coming years. There is often money to be made in finding places with under-valued IP. “Be greedy when others are fearful and fearful when others are greedy.”

Scott pointed to B-round SaaS valuations in excess of $100 million in $15m+ financing rounds with companies with very limited proof of customer traction or revenue. Yet Mark also pointed out that the recent corrections in the public market valuations and the scrutiny new IPOs have undergone is a health sign.

Even though the Initial Public Offering (IPO) alternative for a successful startup seems to be coming back into vogue, it is still extremely rare. companies made the IPO transition in 2009, out of thousands of startups. Only about a dozen U.S.

For angel groups, the distinction between groups and VCs on this issue is dwindling, especially as angel groups do bigger rounds of financing. Note that this applies only to earl stage Series A-type equity financings and assumes no cash dividends are paid to investors. . times the investment.). here of 7.65 [2].

Everyone loves an IPO. Investors see the first issuing of public stock as a way to get in on the ground floor of the next Apple or Tesla. For tech startups , an IPO represents the ultimate validation of their vision — not to mention a prime opportunity to raise enough capital to turbocharge growth. Obstacles to the IPO.

This “overnight success” was first financed in 2004. All have been able to take some secondary stock sales along the way, all remain shareholders of the company and all benefit from late-stage capital provided by Accel, Morgan Stanley, HIG Capital ( Scott Hilleboe ) and others. The abundance of late-stage capital is good for us all.

Next, Mr Blank states, “The LinkedIn IPO valued the company at $8.9 It sent a signal that there is an irrational demand for tech IPOs.&#. Here, he smartly narrows his bubble argument from technology companies to technology company IPOs, because, as I have shown above, there is no technology bubble.

Square filed its S-1 several weeks ago and is now in the middle of its IPO road show process. This past Friday Square also filed an initial pricing range of $11-13/sh which would give them an enterprise value less than their last round of financing ($6B post-money). The post Square IPO: Is Square A Good Payments Business?

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content