This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

At our mid-year offsite our partnership at Upfront Ventures was discussing what the future of venture capital and the startup ecosystem looked like. IRRs work really well in a 12-year bull market but VCs have to make money in good markets and bad. Please follow him & welcome him to Upfront!! It’s just math.

The longer the portfolio maintains the same value without distributing back cash, the worse the fund’s ultimate IRR. This equates to something in the neighborhood of a 10% IRR, which isn’t great given the illiquidity of the asset class and strength of the public markets. So, is this good or bad? LP Constraints.

For the past 10 years, with interest rates near zero, VC investors plowed record amounts into tech startups and enjoyed a seemingly ‘easy’ investing environment. Prices went up from round to round, and startups were encouraged to grow, grow, grow, and not to worry about profitability.

(co-written with Jamie Finney, Founding Partner at Greater Colorado Venture Fund. More and more startups are pursuing Revenue-Based VCs , but “RBI” doesn’t fit everyone. Capacity Capital, Greater Colorado Venture Fund, Indie.VC, Reformation Partners, UP Fund, Versatile VC. Of the Inc. 5000 companies, only 6.5% return cap.

These companies can range from tech startups to food trucks to retail stores. Sohl: “The Angel Investor Market in 2009: Holding Steady but Changes in Seed and Startup Investments”. Villalobos & Payne: “Startup Pre-Money Valuation: The Keystone to Return on Investment” 117. More than 90% of startups fail.[2]

They fail to realize that the considerations are quite different for each, which can make or break their investment efforts, and ultimately their startup. More importantly, the focus on numbers tends to hide other more subjective issues that could be more important for any given startup. How big is your startup opportunity?

Historically, the process of winning capital from limited partners has been opaque. LIMITED PARTNERS’ PERSPECTIVE. As an idea of how high the bar is for a GP, he says , “I dove into our fund log from the last couple of quarters and found that the mean IRR (among VCs listing one) was over 36%.” ” .

———– One of my ex students came out to the ranch to give me an update on his startup. It all starts with understanding what a startup is. What’s a Startup? Just as a reminder, a startup is a temporary organization designed to search for a repeatable and scalable business model. Why small amounts?

They fail to realize that the considerations are quite different for each, which can make or break their investment efforts, and ultimately their startup. More importantly, the focus on numbers tends to hide other more subjective issues that could be more important for any given startup. How big is your startup opportunity?

They fail to realize that the considerations are quite different for each, which can make or break their investment efforts, and ultimately their startup. More importantly, the focus on numbers tends to hide other more subjective issues that could be more important for any given startup. How big is your startup opportunity?

This is the third of three blog posts on financial modeling for startups. The first was on best practices in building financial models , and the second was a template financial model for a startup. Download the Startup Options Valuation model here. Valuing startups is a far fuzzier process. Participa.me

———– One of my ex students came out to the ranch to give me an update on his startup. It all starts with understanding what a startup is. What’s a Startup? Just as a reminder, a startup is a temporary organization designed to search for a repeatable and scalable business model. Why small amounts?

Marty: Welcome to Startup Professionals interviews. Luckily for me (and regardless of what anyone else says, there is a lot of luck involved in angel investing), I have since had significant positive exits to companies like Kodak, CBS and Facebook, and the current value of my portfolio is approaching the 30% IRR that rational angels target.

I entered venture capital with some beliefs – many of which still hold true (such as ‘your LPs are your business partners, not your customers’). Cash flow for small firms in pro rata, bridge rounds, and so on is a real challenge, and it impacts young startups disproportionately.

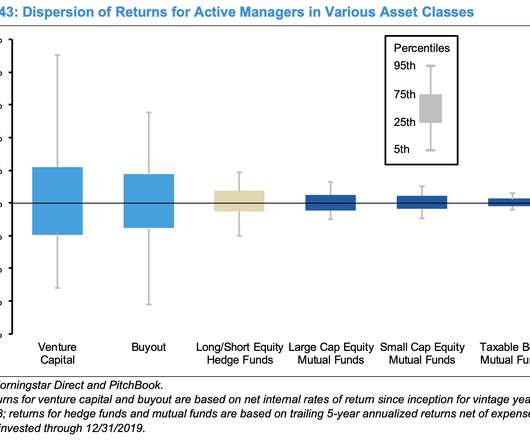

Ian Hathaway, who recently co-authored the second edition of Startup Communities with my partner, Brad, sent me the chart below which highlights how that translates to returns in venture capital as an asset class. If you were going to have several of these, of course, that would work out for your fund. on a gross basis.

I had just left Salesforce.com where I was VP, Products, after they had acquired my second startup. The first check I wrote was just over 10 years ago into a company called Invoca who just announced a new $56 million in funding led by Scott Hilleboe at HIG Growth Partners. Over the past 2.5

They fail to realize that the considerations are quite different for each, which can make or break their investment efforts, and ultimately their startup. More importantly, the focus on numbers tends to hide other more subjective issues that could be more important for any given startup. How big is your startup opportunity?

The companies go through a 3-6 month long startup bootcamp and then typically try to raise angel/seed funding. Most angels invest for a couple of reasons – some do it because they genuinely love the startup space and this is their way of continuing to be involved in a startup, sometimes vicariously.

The $750 million fund combines all of our prior fund strategies – our early stage, early growth, and partner fund investments – into a single fund. When we started Foundry Group, we had four equal partners. We now have seven equal partners. The seven partners all work directly with the companies and partner funds.

The General Partners (GPs) are the operating guys. The money that the GPs and other employees of the firm invest comes from Limited Partners (LPs) — typically the big university endowments, retirement funds, charitable organizations, family offices and high net-worth individuals. This is what makes it more difficult to scale.

Angel investing is an exceptionally high-return asset class; I have collected twelve studies on angel returns in the US and UK, which show median internal rate of return (IRR) between 18 and 38 percent. My proposed model looks a bit like the way many VC funds operate internally, except with far more Partners than normal.

Just look at the disruptive challenges that businesses face today– globalization, China as a manufacturer, China as a consumer, the Internet, and a steady stream of new startups. Perhaps that’s because where established companies might see risks or threats, startups see opportunity. Building Innovation Internally is Hard.

It’s by far the longest time I’ve spent working on any one thing, and I feel very blessed to have been able to work with my partners, colleagues, founders, and collaborators. My partners will tell you that I am an incredibly impatient person. You want someone who will challenge you and be an intellectual sparring partner.

The RBI investor is motivated to help the company grow because that speeds up the pace of revenue payback, and therefore IRR. Keith Harrington, Co-Founder & Managing Director at Novel Growth Partners, writes, “RBI may not work for a company with a super high growth trajectory, because the payments could be very large”. .

It’s by far the longest time I’ve spent working on any one thing, and I feel very blessed to have been able to work with my partners, colleagues, founders, and collaborators. My partners will tell you that I am an incredibly impatient person. You want someone who will challenge you and be an intellectual sparring partner.

It’s by far the longest time I’ve spent working on any one thing, and I feel very blessed to have been able to work with my partners, colleagues, founders, and collaborators. My partners will tell you that I am an incredibly impatient person. You want someone who will challenge you and be an intellectual sparring partner.

When I was where you are, 36 years ago (can ya believe it) I didn’t have a plan—but I did have an aspiration: I wanted to go to Silicon Valley and I wanted to work in startups. Eventually I left Oracle, wanting to do another startup. Problem is, startups that have world changing potential are not that easy to find.

Or if you’re a VC raising from LPs you have to list all of your deals, your investment value, your carrying value, your multiples, your IRRs, TVPIs, DPIs, etc along with net cashflows plus your previous LPAs. I never thought of this until I became the Founder & CEO of my first startup company. Some people find this elitist?—?I

In February of last year, Fortune magazine writers Erin Griffith and Dan Primack declared 2015 “ The Age of the Unicorns ” noting — “Fortune counts more than 80 startups that have been valued at $1 billion or more by venture capitalists.” Next came Rolfe Winkler’s deep dive “ Highly Valued Startup Zenefits Runs Into Turbulence. ”

It takes a long time to see the results of a startup that does well. A common intermediary milestone for most investors is IRR (internal rate of return) of the fund. So there are a lot of unrealized gains built into the IRR of an early fund. Company progress on KPIs, including revenue, typically do not get factored into IRR.

Some of the firm’s partners may move on to new jobs during this phase but at least some are usually still around. 4) VCs Keep Quiet About Fading Away - As described above, VC firms usually die gradually and quietly rather than spectacularly and publicly as is sometimes the case for startups. So at a fund level (e.g.

You don't want the "average" fund, because average funds don't do well--just like you don't want to model the average startup, because you might as well draw a big flaming hole in the ground. Do seed investors have Limited Partners with different return expectations than Series A and beyond investors? Time is the enemy of IRR.

OH in South Park, San Francisco (or on Zoom from Big Sky, Montana): “OMG, crazy – that firm just paid 100x revenue to invest in [insert hot startup here] – what could they be thinking?” Not too shabby! Ultimately, determining a valuation is a delicate balance between many factors.

Blue Future Partners, a venture capital fund of funds, recently interviewed me on ESG in venture capital. I’m also incubating a startup, Action Tank , to help other NGOs accomplish their goals using their supporters’ unique expertise. Concentration in consumer/branded products startups. Why is that? Firm revenues.

We figured that given their commitment to the asset class, so long as we did our job well and treated them like partners in our business, they would show up each fund to back us. No reason to sell winners prematurely just because of original fund length, especially given our LPs are largely cash-on-cash return focused more than IRR.

I was comparing my small personal angel portfolio and my investments at 500 Startups, and I noticed that on a percentage basis, the companies in my personal portfolio have been able to raise more money on average and more easily than companies in my 500 portfolio. It really pains me to write this post…but it has to be said. Why is that?

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content