This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In case you don’t know – as VCs we have have 2 sets of customers: LPs (limitedpartners) who invest money in our funds and entrepreneurs (who we in turn give money to and help support them in building businesses we hope will be valuable).

These studios have different metrics than startup studios whose limitedpartners are private family offices or venture capitalists. In both North America and Europe, many venture studios in non-major cities are funded by government agencies to stimulate local growth, at times with matching donations from companies.

In recent years we’ve had big wins across all of our long term partners (Yves: Envestnet), (Steven: TrueCar), (Me: Maker Studios). For some reason that I haven’t yet figured out, LimitedPartners seems to be pretty confidential about which firms they’ve invest in. Who gave you the money?

LimitedPartners or LPs (the people who invest into VC funds) have taken notice as 2014 is by all accounts the busiest year for LPs since the Great Recession began. But it still takes VC to scale a business (thus large capital into industry winners like Uber, Airbnb, SnapChat, etc).

The VC industry grew dramatically as a result of the Internet bubble - Before the Internet bubble the people who invested in VC funds (called LPs or LimitedPartners) put about $50 billion into the industry and by 2001 this had grown precipitously to around $250 billion. Here’s my take: 1.

You charge your limitedpartners this, but you have to pay it back before you start taking a cut of the profits. Most larger funds have a fee around 2%, but when you''re this small, you need a little bit extra to keep the lights on. It''s only a little bit of a performance drag, though, because management fees act like a loan.

What will matter are: whether the people who invest in VC funds (LPs or LimitedPartners) increase their activity and the performance of that actual fund. What the LPs will be looking for are VCs with enough “exits&# to prove that they can make returns.

Almost all of this increase came from our existing LimitedPartners, with a small portion that was made available to new LPs. As always, we are grateful for the partnership of all of our LimitedPartners who entrust us to be good stewards of their capital in both good markets and bad.

Finally, as an innovation ecosystem (VCs, their limitedpartners, and startups) we need to do a better job in insisting in transparency in government, calling out rent seekers and regulators who no longer regulate, and try to keep government from premature regulation of new innovation.

By contrast, they backed 620 funds in the last three months of 2021 First time fund managers hit hard: In 2022, limitedpartners backed 141 funds run by first-time managers, a 59% decline from the prior year and the lowest number since 2013 How does the constrained LP environment manifest for funds and startups?

All were backed based on the sole criteria that they had the potential to make my limitedpartners a lot of money. Three teams have African-American founders. Three of the founding teams are married couples. The diversity is the direct result of our mission—to build the most accessible venture capital fund in NY.

People all across the value chain have taken notice including LimitedPartners who are the people who invest in VC funds in the first place. Why prorata rights are now sought out by LPs.

VC’s raise money from their investors (limitedpartners like pension funds) and then spread their risk by investing in a number of startups (called a portfolio). BTW, Angel investors do not have limitedpartners, and often invest for reasons other than just for financial gain (e.g., The Deal With the Devil.

Leveraging the multi-industry expertise of its limitedpartners to define targets, grow companies and enhance returns, Hauser Private Equity makes partnerships via control buyout funds, as well as managers of growth equity and special situations funds.

Build the firm as much as possible before you solicit limitedpartners. . Your materials should ideally meet the expectations of the Institutional LimitedPartners Association, even if you’re not targeting institutions. Note that limitedpartners view formatting as a proxy for professionalism.

The trends described above in VC performance have an upstream effect on LimitedPartners which is somewhat counter-intuitive. This data seems to line up with the narrative I’m hearing on the ground. . LP Constraints. Most LPs are trying to manage some targeted asset allocation.

If you were a “with it” VC you needed to have a “Content&# or “Multimedia&# company in your portfolio to impress your limitedpartners – educational software companies, game companies, or anything that could be described as content and/or Multimedia. Not all VCs are equal.

The LimitedPartners (LPs) who back funds don’t expect their dollars to be passive. Another reason is that your C-round of capital may very well be $25–100 million and at those check sizes investors want to have an independent board at a minimum (many boards are 3–2 or even 4–1 investors to founders).

Historically, the process of winning capital from limitedpartners has been opaque. LIMITEDPARTNERS’ PERSPECTIVE. Origins is a podcast about LimitedPartners, created by VC Notation Capital. Denis Tse: Fund Management Craftsmanship: An LP’s Food for Thought for Emerging VC General Partners.

I would argue that returns might go up if VC fundraising was a lot more meritocratic and if the big LimitedPartners got to see everyone who was fundraising at the same time. Everyone would know who they were and they could have a short form that you could apply to pitch your fund to for free? For myself, I've been lucky.

Now, funds do work to charge some of these costs back to their portfolio companies, but usually these offsets flow to the fund’s General and not its LimitedPartners. All this work is necessary to do venture capital right, but is also expense and friction filled. So what to do?

If you’re a venture capitalist … you have limitedpartners that give you money to invest on their behalf, and you’re responsible for giving them outsize returns. Steve : And they wanted a bigger business than just a vent company. Nayeem : (Nods.)

Limitedpartners (LPs), who manage the capital that gets deployed into venture capital funds, can play an important role in diversifying the funding landscape. Limitedpartners are pension funds, university endowments, funds of funds (who get their money from pension funds), family offices and foundations.

Most VCs (including ff Venture Capital ) collect money from independent limitedpartners in order to form their fund. This is not a comprehensive list, but merely an attempt to highlight some of the most notable examples relevant for technology-enabled startups. 1) Corporate Venture Capital.

Their fiduciary responsibility was to manage a portfolio of investments for their limitedpartners. At the end of the day VC’s have to provide their limitedpartners with great returns or they aren’t going to be able to raise another fund. If you succeed so do they.

At the Upfront Summit in early February, we had a chance to have many off-the-record conversations with LimitedPartners (LPs) who fund Venture Capital (VC) funds about their views of the market.

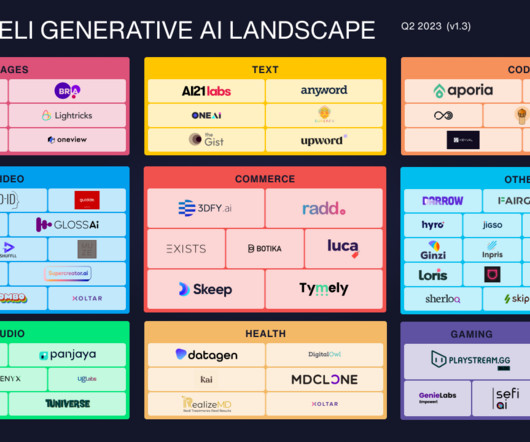

Several of our limitedpartners are media and entertainment strategics: broadcasters, publishers, telcos etc, so content creation, distribution and monetisation has always been close to our core focus. At Remagine Ventures we started investing in the generative AI space very early back in 2019.

Similarly, our limitedpartner investors have their own due diligence standards, and we manage HOF Capital to keep in line with their standards and expectations. Ask on what KPIs each Partner is evaluated. The post LimitedPartner Due Diligence on Venture Capital and Private Equity Funds appeared first on David Teten.

Similarly, our limitedpartner investors have their own due diligence standards, and we manage HOF Capital to keep in line with their standards and expectations. Ask on what KPIs each Partner is evaluated. The post LimitedPartner Due Diligence on Venture Capital and Private Equity Funds appeared first on David Teten.

VC’s invested their limitedpartners’ “risk capital” in a portfolio of startups in exchange for illiquid stock. Some of the old-line venture firms have changed their strategy, but some are still locked into last decade’s model while the partners are living off of their management fees and go through cargo cult like rituals.

You will work closely with Joshua Baer, Gordon Daugherty, Bryan Chambers, the Ventures Team, limitedpartners, external venture capitalists, lawyers, accountants and startup CEO’s to review legal agreements, perform our diligence checklist, and make sure transactions close in a timely manner.

I cant tell you how many times I got announced as a successful VC when I was introduced on a panel or sat across the room from a potential limitedpartner telling them I was. This is what I know it feels like for a lot of founders and investors alikefloating in the rarified air of extremely successful people defined by their outcomes.

A more efficient approach is to mine the data exhaust from the LimitedPartner universe to identify those LPs most likely to find your fund attractive, and focus all your energy on them. Relationship Science makes it easier to understand and map social networks into potential limitedpartners. 2) Raise capital.

Her responsibilities included: strategic counseling, business modeling and deal negotiation for the various for medical startups in the portfolio and is a limitedpartner at NGT3 Medical Accelerator in Israel. Sablotsky continued her professional career as Vice-President of Portfolio Development for Jacobs Investments, LLC.

I’ve lately been attending meetings with our shareholders (called LPs or limitedpartners). We didn’t realize.&# If you can get away with it, go for it. Sitting by the screen is the best excuse. I’ve learned that LPs don’t expect presentations to be done on a screen so I need to travel around with paper.

Either way, VC funds aren't really built around creating much of an experience for their LimitedPartners. Other times, they might not even let individuals participate in future funds at all. For smaller funds, I think this is a real mistake.

A more efficient approach to fundraising than haphazard networking is to mine the data exhaust from the limitedpartner universe to identify those LPs most likely to find your fund attractive, and focus all your energy on them. Cobalt for General Partners helps GPs to optimize their fundraising strategy.

This investor decided to use the fact that they got into a company that appears to be doing well to their benefit to almost fraudulently persuade limitedpartner investors to give them money.

And they have a fiduciary responsibility to their own limitedpartners.) You may like them and they might like you, but they have a fiduciary duty to the shareholders, not the founders. That means the board is your boss, and they have an obligation to optimize results for the company.

But through expressing points-of-view I can raise above the consciousness of my customers (entrepreneurs and limitedpartners who invest in VC funds) in ways that I couldn’t without breaking through the noise of the hundreds of others of VCs who also have money. Think about Luma Partners. I am a VC. I hand out money.

Limitedpartners, who commit capital to venture funds, have to commit for 7–13 years. This model has other problems. By far the largest is illiquidity. Once a venture investment is made, the fund will not realize a return until the company sells or IPOs. Few investors can afford to think on that time-scale.

I have a draft deck put together for a next Brooklyn Bridge Ventures fund. I pretty much hate it. Don't get me wrong--the numbers look great. That's not it. It just doesn't really get at what's really important. I wasn't sure exactly how it missed, so I went back to first principles. What *is* really important for a venture fund?

Those incentives are often misaligned with the interests of founders and limitedpartners. Individuals get promoted for successfully out-competing other investors and winning over founders long before knowing whether those were great investments to make.

The general partners of a venture capital fund make money… …by raising the bulk of the capital that the fund’s investable capital from “LimitedPartners”, usually institutions such as university endowments, insurance companies and pension funds. This is the money that is invested into the startups.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content