This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A version of this article is in the Harvard Business Review. — Unremarked and unheralded, the balance of power between startup CEOs and their investors has radically changed: IPOs/M&A without a profit (or at times revenue) have become the norm. 20th Century Tech Liquidity = Initial Public Offering.

A version of this article first appeared in the Harvard Business Review. For most startup employee’s startup stock options are now a bad deal. Why Startups Offer Stock Options. But 21st century companies face compressed technology cycles, which create the need for continuous innovation over a longer period of time.

People buy companies for 3 primary reasons: 1) they want the management team / talent 2) they want the technology or 3) they want the market traction (revenue, customer base, profits, etc). The downside is that people need to buy their stock. In fact, far better if you haven’t raised venture capital. Do it early.

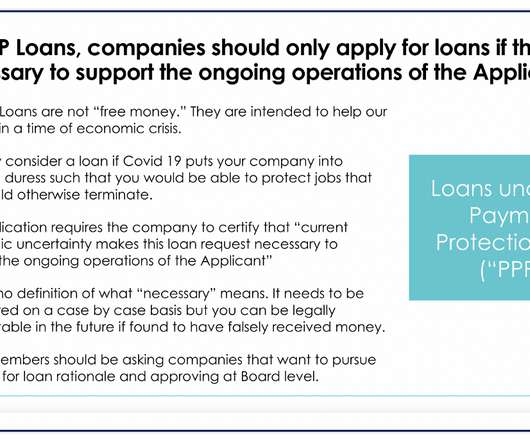

This money is administered by the SBA (small business administration) and is obtained through an approved bank who reviews your application. It’s slightly harder if you’ve only done an A-round and therefore have just one VC around the table who owns more than a majority of the preferredstock. payroll protection.

I’ve been writing up reviews of this season’s Shark Tank pitches from a silicon valley VCs perspective. Week three’s breakdown covered topics like how hard momentum is to turn around, and how participating preferredstock works. They won a design award at a trade show, but have no revenue and no orders.

A new wave of Revenue-Based Investors are emerging who are using creative investing structures with some of the upside of traditional VC, but some of the downside protection of debt. I believe that Revenue-Based Investing (“RBI”) VCs are on the forefront of what will become a major segment of the venture ecosystem. He said, . “[W]e

In fact, SaaS industry revenue is projected to grow from $49 billion in 2015 to $67 billion in 2018, a compound annual growth rate of approximately eight percent. At this stage, simply list your primary revenue streams and your key expenses. At this stage, simply list your primary revenue streams and your key expenses.

Every successful technology company raises money throughout its lifecycle, perhaps starting with a seed investment and progressing through Series A, B, C, late-stage investments, and, for the most successful companies, an IPO. These large, high-priced private financings are the defining characteristic of this particular technology cycle.

3] However, if they are built bottom up, they demonstrate and make explicit a range of business model assumptions the entrepreneur is using to think about his business and its revenue model. Term-sheets for preferredstock offerings are designed to protect the investor in case things don’t go as well as planned.

Dual-class voting structures are receiving a lot of attention these days along with intense publicity related to the Facebook IPO , following in the wake of other recent tech IPOs with a similar structure such as Zynga and LinkedIn. Options and warrants, when issued, are also typically exercisable for shares of Common Stock.

AGILEVC My idle thoughts on tech startups. Now that Google’s acquisition of ITA is closed, following lenghty FTC review, it would appear Kayak is poised to proceed with their IPO in the coming months. =. Financial Snapshot: 2010 Revenue: $170 million. Revenue growth: 51% YoY (2010), 1% YoY (2009), 131% YoY (2008).

I wassurprised recently when I realized that all the worst problems wefaced in our startup were due not to competitors, but investors.Dealing with competitors was easy by comparison. There never has to be atime when you have no revenues. I dont mean to suggest that our investors were nothing but a dragon us. Whendel.icio.us

The firm attracts deal flow by promising a decision (positive or negative) in under 2 weeks, with minimal paperwork and without repeating duediligence. Coinvestors need to figure out ways to prioritize themselves in a VC’s preference stack for syndicating opportunities. – Launch a “ venture studio ” or “ foundry ”.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content