This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The market was down considerably with public valuations down 53–79% across the four sectors we were reviewing (it is since down even further). ==> Aside, we also have a NEW LA-based partner I’m thrilled to announce: Nick Kim. But rest assured valuations get reset. And reset they must. It’s just math.

In 2011, the valuation of pre-revenue, start-up companies is typically in the range of $1.5–$2.5 Working within a network of angel investors also expands the pool of expert resources and helps divide the work of screening companies and investment duediligence. Scorecard Valuation Methodology.

As a frequent advisor to new entrepreneurs and startups, I often hear your frustration with being treated differently from other startups by investors, on expectations for valuation , traction, and market size. Valuations here are always low, and funding generally depends on friends and family, or a few forward-thinking angels.

There has been a lot of chatter regarding changes in revenue recognition criteria lately, but the effects it will have on the evaluation of companies planning an exit is just beginning to emerge. Specifically, the new standard will follow a five step model for revenue recognition: Identify the contract (the deal that has been reached).

I have been close to the tech & startup sectors for more than 20 years and I can’t think of a period in which I felt more optimistic about the innovation and value creation I see in front of us. From this we have seen a commensurate boom in the number of startup companies. They compete on features, price and execution.

This is the first of a six part series on different methods used by angel investors to arrive at pre-money startup valuations. It is one of the most useful methods for establishing the pre-money valuation of pre-revenue startup ventures. Return on Investment (ROI) = Terminal (or Harvest) Value ÷ Post-money Valuation. (in

I think it’s important for enterprise startups to layer in professional services into your revenue stream. deliver profitable revenue that while on gross margins of 50% vs. software at 85-95% it is still profits to help you cover fixed costs. Control Size of PS Revenue Relative to Software Business. rollout support.

A version of this article is in the Harvard Business Review. — Unremarked and unheralded, the balance of power between startup CEOs and their investors has radically changed: IPOs/M&A without a profit (or at times revenue) have become the norm. 20th Century Tech Liquidity = Initial Public Offering.

You can read various articles out there which will give you the cursory facts about Airbnb like their overall revenue or profitability or how their business has faired here in 2020 in the COVID environment. But ops & customer support is another 17-20% of revenue and arguably you couldn’t run the business if you took that away.

2 preamble issues having read the comments on TC today: 1: I know that the prices of startup companies is much great in Silicon Valley than in smaller towns / less tech focused areas in the US and the US prices higher than many foreign markets. As the risks below get eliminated the higher the valuation investors are prepared to pay.

Ah, but today’s Internet companies have real revenue! Responses ranged from, “hey, they’re in a HUGE market&# to “it is an amazing company and their technology rocks.&# For others it feels like a two-speed economy, where rules apply to hot tech startups that don’t apply elsewhere. and profits!

How could Bird really be worth the reported $2 billion valuation that I read about in this press? While I promised not to comment on the exact valuation you can assume that it is very large and perhaps the fastest rise from zero to what some have called a “unicorn” valuation. Forget the valuation?—?I Not really.

This is a very introductory place to start, but if your company owns the building, machinery, inventory, and/or technology in which it uses to operate, there is often significant value in this in and of itself. Look at Revenues. Figure Out the Net Assets of the Business. If your company is worth only $2.5

Revenue multiples, profit multiples, premium over the previous financing — these are metrics used by sellers to help determine a minimum acceptable price. Even for startups, it takes years for a new product to become good enough to demand many millions of dollars in revenue.). Yet mobile advertising revenues were paltry.

Nearly every successful tech startup I’ve observed over the past 20 years has gone through a similar growth pattern: Innovate, systematize then scale operations. An example of the systems companies build are pricing & revenue management tools to best help to optimize yield. Seriously, this happens.

This article originally appeared in the Harvard Business Review. As more and more companies face disruption from globalization, new technology, and startups that have more capital than the incumbents, the continuing cry from Wall Street investors is, “Why can’t companies be as innovative as startups?”.

Posted on September 14, 2009 by steveblank Over the last 30 years Wall Street’s appetite for technology stocks have changed radically – swinging between unbridled enthusiasm to believing they’re all toxic. While there was an occasional bad apple, the public markets rewarded companies with revenue growth and sustainable profits.

Valuations were enormous relative to progress in companies. Companies with less than $2 million in revenue were asking for $50-60 million valuations and getting them. I spent my days meeting companies, figuring out what areas of the market interested me and trying to get a sense for how VCs thought about fair valuations.

Consumer spending is 70% of the economy and will continue to be stretched – We can look all we want at tech innovation, VC funding cycles and hot M&A deals, but ultimately growth and therefore investment must be underpinned by revenue. This has a tangible impact on the valuation of start-ups and the pace of investment.

You get to have interesting conversations with founders and review business plans and then see how these businesses evolve over the years. " Revenue doesn't pay your bills, GM does — @msuster 2/ Founders obsess with revenue as a vanity metric. Things happen, people tire, sometimes tragedies.

especially if the startup already has a product and revenue? Everyone moved to earlier stage – part of the decline in late stage investing is the ‘baggage’ of companies that previously raised money at inflated valuations that they would struggle to justify in today’s market.

We realized that past K-12 Entrepreneurial classes taught students “the lemonade stand” version of how to start a company: 1) come up with an idea, 2) execute the idea, 3) do the accounting (revenue, costs, etc.). These two startups had problems they could not solve on their own due to lack of resources—time, people, money.

Just don’t quit your day job before your new company is producing revenue. Use this approach before you have a real valuation, a real product, or any real customers. This source often gets overlooked, but it should be a major focus these days due to government initiatives on alternative energy and technology.

We received so much positive feedback from our This Week in Venture Capital show walking through valuation calculations & term sheets that we decided to do a Q&A show this week to address topics that entrepreneurs want to learn about. The best thing to get is a “right sized&# valuation. A: It’s not best.

Due to the struggling economy as well, traditional individual Angel investors haven’t been able to fill the gap. It’s higher risk, but higher return, to pick the big winners early, before Angels have set unreasonable valuations and restrictive terms. Technology costs are plummeting, meaning you can do more with less.

I conclude that the genesis of this trend seems to come from several forces, including the following: Less investment capital available due to the recession. Due to the economy as well, traditional individual angel investors haven’t been able to fill the gap. Technology costs are plummeting, meaning you can do more with less.

are eliminated during duediligence. It should answer every question an investor or associate might ask, including current valuation, funding needed, and exit strategy. In most cases, a Microsoft Excel spreadsheet is adequate, with projection formulas for revenue, costs, and cash flow over the next five years.

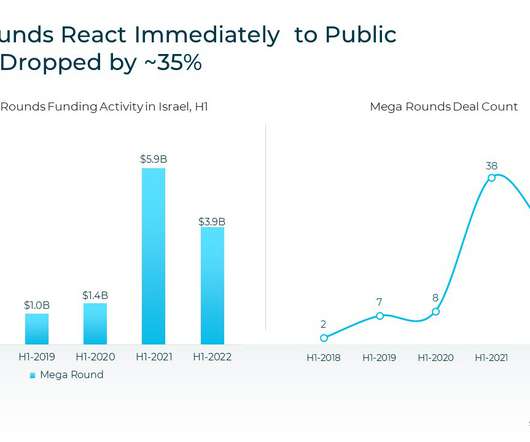

In the big picture, it’s needless to say that the market is going through a challenging economic period, but despite tech layoffs and a decline investments in Q2 2022 (as was seen in the US) the Israeli tech industry faired well. IVC/Leumi Tech Israel techreview Q2 2022. billion in revenue in 2021.

These shortcuts add up and become what is called technical debt. You fix technical debt by refactoring , going into the existing code and “cleaning it up” by restructuring it. to drive traffic to their site, which they then turned into ad revenue. Organizational debt was coming due. Refactoring” organizational debt.

Just don’t quit your day job before your new company is producing revenue. Use this approach before you have a real valuation, a real product, or any real customers. This source often gets overlooked, but it should be a major focus these days due to government initiatives on alternative energy and technology.

When expanding their businesses, most tech startups and the subindustries that comprise the tech industry typically follow this model. Analysts perform a valuation of the company in question before the beginning of any round of funding. What is the Evaluation of the Funding?

In order to avoid formal valuation report costs, shareholders utilize benchmarks of the industry and rules of thumb to estimate the ballpark values of their interests. This article will cover all about the rule of thumb business valuation approaches, when to use them, and their pros and cons. Rules of thumb and business valuation.

To grow your brand and increase revenue, here are some handy tips on how to optimise your affiliate marketing strategy. You need to know the risk factors when picking affiliate partners, otherwise you run the risk of losing revenue. These can include webinars, email marketing , product review blogs, and creating YouTube videos.

They should heed the age old advice that raising slightly more money while you can is always better than trying to optimize future valuations. Should VC’s really be impacted by public market valuations when the money that they’re investing today should be for returns in 7-10 years? Short answer – yes.

I received an email last week from an entrepreneur (let's call him Mike) Now to begin, I was pretty impressed with Mike since he used a nice technique to get his email in my inbox (due to the volume of emails I receive, they are screened by others before they get to me). Getting a $100 Million valuation is impossible for a startup.

are eliminated during duediligence. It should answer every question an investor or associate might ask, including current valuation, funding needed, and exit strategy. In most cases, a Microsoft Excel spreadsheet is adequate, with projection formulas for revenue, costs, and cash flow over the next five years.

Yet 2013 is still projected by The Fiscal Times as a difficult IPO opportunity for startups, due to choppy markets, continuing fiscal uncertainty, and the Facebook fiasco. Your friends and family are really the only answer until you have a significant revenue stream. Identify the right people in the right venture firms.

investors the opportunity to participate in the Israeli high-tech market. based Angel capital with early stage technology companies in Israel, and do so in a way that substantially mitigates the risk of seed stage investing. Janvest: In 2009, roughly 450 Israeli high-tech companies raised a little over $1.0B.

But by the time we ended 2015, the headlines like “ The Dangers Ahead if Tech Unicorns Get Gored (WSJ) ” and “ Regulators Look Into Mutual Funds Procedures for Valuing Startups (WSJ) “ “Unicorn” went from being a brass ring to reach for to a term used with sarcasm or derision. Revenue is revenue, right?

The Risk Factor Summation Method the fifth methodology for estimating the pre-money valuation of pre-revenue companies we have described in recent posts. Readers may have noted that both the Scorecard Method and the Dave Berkus Method considered a narrow set of important criteria for investment in arriving at a pre-money valuation.

When I met my now-wife, I realized that any technology that can find me a spouse is a killer app. I’d argue that the same type of technologies that have revolutionized dating can revolutionize our industry. . I walk through below how progressive investors are using technology and analytics throughout all of their operations.

At today's roundtable we had some interesting companies and a lot of fundraising discussions, and I will review them shortly. As a thumb rule, try to get enough validation so that you can get to at least a $2 million pre-money valuation before raising equity capital. Bottom line, early stage equity is very, very expensive.

Billion in investments across a range of industries, including technology, sustainability, traditional and alternative energy, mining, construction services, transportation, and healthcare. Are there new revenue streams you can tap into? The firm has made more than $4.5 It is also the time to take a hard look at your business model.

90 Things I’ve Learned From Founding 4 Technology Companies. On October 27, 2010 I wrote a blog post about the “ 57 Things I Learned Founding 3 Tech Companies.”. 90 Things I’ve Learned Founding 4 Tech Companies: Find your company’s One Thing. ?? We do twice-yearly reviews of all Fab team members. So, here goes.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content