This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

. “Whenever I hear advice about pricing a round too high for the next round, I can’t help but think: well, if the choice (ceteris paribus) is between. I would love it if other people would weigh in on the comments section below if you’ve had experiences with downrounds. A downround.

Many companies are now having to resort to tough measures in order to stay afloat, including layoffs, downrounds and tough terms from current investors. If the answer is yes, then a downround is likely the best path forward. Why you shouldn’t worry about raising a downround ( source ).

The A round was done in February 2000 (end of the bull market) and my B round was done in April 2001 (bear market). As a result I had to do a downround. Downrounds are psychologically really difficult on companies and can make it harder to do later rounds. I eventually needed more money.

Even if you have an interesting story to tell most investors won’t want to go through the brain damage of doing a “ downround ,&# which creates tension between them and early investors. They get a cheaper price, they wipe out much founder stock value and they reissue you new options.

She has a good article today in TechCrunch titled Embrace the downround (it’s going to be okay, maybe). ” Now, I’m not encouraging anyone to do a downround if unnecessary., ” Now, I’m not encouraging anyone to do a downround if unnecessary.,

Don’t assume that you can “just do a downround” if necessary. Downrounds are corrosive. So if your fund raising isn’t moving consider lowering price to shore up your balance sheet and reduce risk. Optimize for a W more than % dilution in these circumstances. Insiders hate them and fight them.

New investors hate downrounds. They will enter the “triage phase&# of the market where they figure out which of their existing deals will survive. Many good companies will not get funded. Vultures will start circling looking for deals. Get funded now, if you can.&#. That’s a fact.

In times when venture capital is hard to get, investors extract high costs for failure (down-rounds, cram downs , new management teams, shut down the company.)

The result is mass layoffs (over 119,000 in the US since the beginning of 2023 and it’s only Feb), downrounds (even for Silicon Valley darlings like Stripe) and fund terms that go above the 2/20 standard. Gil Dibner captured that sentiment in a recent Twitter thread: We talk to a fair number of LPs.

Carta reports that 20% of the rounds in 2023 were downrounds, but I believe the actual number is much higher. For that and other reasons (like cash preservation) VCs moved to focus more on earlier stage, and many funds that typically invest in A started deploying more into seed rounds.

new unicorns created each day), startups may find themselves raising downrounds as they struggle to justify previous valuations. But the valuations weren’t necessarily given as a function of revenue, and often with multiples on ARR that we don’t see in today’s market. With over 1,000 global unicorns (and about 1.5

How You Get Slaughtered in a DownRound: When Taking Venture Capital Doesn’t Go as Planned – crowdspring.co/MvF29W. Facebook and WhatsApp: The Nineteen-Billion-Dollar App – crowdspring.co/1jOdRlK. DHL Pranked UPS Into Advertising For Them – crowdspring.co/1jOeA6v. “If you want to sell ads, sell ads.

Has there ever been a downround, inside round, a flat round, or a CEO change? While the actual answer to this question won’t necessarily provide a definitive answer about the ability for the company to access both cash and additional capital, it will open up a discussion about it.

Many startups that raised money in 2021 on inflated valuations that were detached from their actual value, are struggling to raise up-rounds and face difficult choices these days: downrounds, early sellout or failing altogether. A good way to think about valuation in seed/pre-seed is to reverse engineer the next round.

For the common shareholders (employees, advisors, and previous investors), a cram down is a big middle finger, as it comes with reverse split – meaning your common shares are now worth 1/10th, 1/100th or even 1/1000th of their previous value. (A A cram down is different than a downround.

As Cuban pointed out, this is a “downround” Zomm is seeking $2M for 10% of the company, implying an $18M pre money valuation today. Some partial answers came up, including spending on a new version of the product with additional features, and excessively high inventories relative to actual sales in holiday 2011.

Then, if you end up doing a downround, it suddenly matters a lot. Don’t worry about this too much, until you do a downround. Then use the downround to clean up your preference overhang. The post Founders – Use Your DownRound To Clean Up Your Cap Table appeared first on Feld Thoughts.

Unreasonably high early valuations hurt the entrepreneurs, as well as professional investors, later when a second round becomes a downround or can’t be negotiated. A startup that is listed on a crowdfunding platform gets no formal pushback or negotiation on its declared valuation.

But, in subsequent rounds of funding inflated valuation will be normalized resulting in a downround. You might have seen that valuations of several unicorns were suddenly slashed down. Point number 3: Never raise money with an increased valuation. It might be tempting to do so.

Consequently, some startups have faced struggles securing investments, resulting in downrounds where their valuations decline between funding rounds. Additionally, these downrounds can decrease employee morale, as they may dilute shares or pay cuts, affecting the overall work environment.

In VC: I see a fair number of deals that have reached some point of stagnation that are seeking a flat or downround. “The most important thing to do if you find yourself in a hole is to stop digging.” . This is bad. Tread very carefully. . 4) High Concentration of Investments - Berkshire Hathaway is massive. And yet, Mr.

Of course valuation is in the eye of the beholder but if that VC thinks your last round valuation was way too high then he or she is more likely to politely pass rather than try and talk down your valuation now. VCs hate “downrounds” and many don’t even like “flat rounds.” There are some simple reasons.

This clause attempts to protect the conversion price of stock of angel investors, prior to additional financing, from being reduced to a price equal to the price per share paid in a later “down” round. But some dilution is almost inevitable. Right of first refusal.

This clause attempts to protect the conversion price of stock of Angel investors, prior to additional financing, from being reduced to a price equal to the price per share paid in a later “down” round. But some dilution is almost inevitable. Right of first refusal.

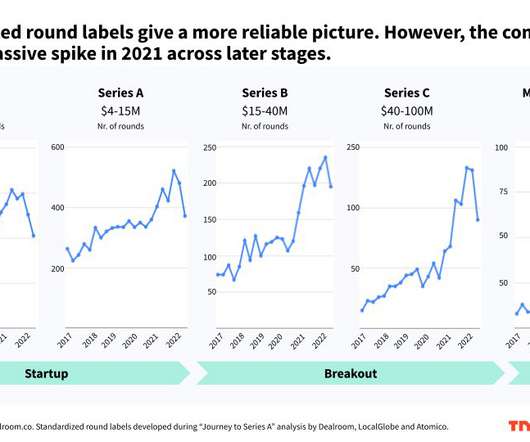

As Fred Wilson put in in his post ‘What will happen in 2023’ “I believe that ‘new normal’ is more or less where we were in 2015 where seed rounds were done around $10mm, A rounds were done around $15mm to $25mm, B rounds were done around $25mm to $50mm, and growth rounds had a cap at 10x revenues.”

According to Barry Kramer, a partner in the firm and a co-author of the survey, during the third quarter, "up rounds exceeded downrounds 52% to 30% with 18% flat.

Unreasonably high early valuations hurt the entrepreneurs, as well as professional investors, later when a second round becomes a downround or can’t be negotiated. A startup that is listed on a crowdfunding platform gets no formal pushback or negotiation on its declared valuation.

Why DownRounds are Harder Than You May Think. Downrounds are hard. A slight downround is achievable but massive “hair cuts” are very hard to do. Also, new investors will be worried that the downround will cause founders or senior management to depart and no VC wants to replace management.

If you do a $1 million angel round at $6 million pre-money and hope to do a Series A round for $2-3 million that’s fine as long as you’re doing awesome against your metric goals and the market continues to be frothy. If either condition doesn’t hold it will be hard to do anything but a flat or downround.

This clause attempts to protect the conversion price of stock of angel investors, prior to additional financing, from being reduced to a price equal to the price per share paid in a later “down” round. But some dilution is almost inevitable. Right of first refusal.

Given that the Series Seed is issued at a fairly low valuation, anti-dilution protection is probably not that important, as a “downround&# from a low valuation in the Series Seed is unlikely. Deleting anti-dilution rights saves several pages of text in the Certificate of Incorporation. Comprehensive protective provisions.

Israel’s most promising startups in 2024, according to Israeli news website N12 News Israel Are we past the worst in downrounds? Data by Carta shows that the downround percentage for Series A through Series D fell from Q1 to Q2 of this year. AI and all the rest. 35% of U.S.

I always caution entrepreneurs not to take too high a valuation in any round because it sets very high expectations for the next round. A downround, which can damage a company and make it difficult to raise money in the future. Unfortunately, most startups don’t meet their initial rosy projections. What happens then?

Unreasonably high early valuations hurt the entrepreneurs, as well as professional investors, later when a second round becomes a downround or can’t be negotiated. A startup that is listed on a crowdfunding platform gets no formal pushback or negotiation on its declared valuation.

Many startups extended runway, cut costs and took on painful downrounds or expensive debt to avoid raising in 2023. However, there’s a light at the end of 2024 You can tell the market doesn’t believe that we’ve hit rock bottom yet. Those ‘band aids’ are running their course and it might get worse (i.e.

. $10,000 is a round number and that means that it is not specific. The client is either going to figure you have no real idea what something costs, or that you’re rounding up in anticipation of expecting to be negotiated down. Round numbers are “ball park numbers.”

Here are the top things I hear about follow ons and why they don't make a lot of sense to me: 1) You need to have follow on capital to protect your investments in case of a downround. If you're doing seed deals, how often does a downround in a seed deal even happen? Down from what?

Also, they have a strong belief that any sign of weakness (such as a downround) will have a catastrophic impact on their culture, hiring process, and ability to retain employees. Their own ego is also a factor – will a downround signal weakness?

If a company raised a big B and/or C round and needs more money the late stage guys have the bucks and that early-stage guys often don’t. So in companies with high burn rates you can find the following: Seed funds wanting to sell the company / get a return or growth investors pushing for a recap or massive downround.

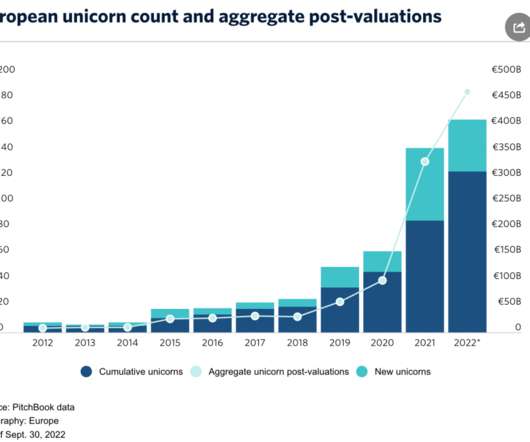

Atomico’s founder Nicklas Zennstrom recently called the end of the high valuations era and urged founders and VCs to remove the stigma from downrounds. It’s enough to take a look at the global unicorn club of 1,191 startups valued at $1 billion or above to understand that challenging times are ahead for many of them.

This combo all too often leads to various forms of deal unpleasantness, like cram-downrounds, liquidation preferences, and change of control provisions, which in turn, often lead to unhappy founders and angel investors even in somewhat successful exits. And they hire very aggressive securities attorneys to represent their interests.

Restructures, DownRounds, and Pay to Plays. Whatever gets reported is just the tip of the iceberg. The reality is lots of companies – many of them quite promising – have already undergone, or will be facing, next financings which “clean up” old cap tables.

Hopefully, it’s in high demand for good reasons, otherwise you risk a downround in the future. The latter won’t be enough money to grow and without the capital to grow, could risk failing or a downround. Don’t risk a downround. This method of valuing a company is further from reality than most attributes.

If so, the VC will contemplate a “downround” – that is: offering an investment where previous investors find their investments instantly worth less than their original value, even if the investments were made at high risk and years earlier.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content